With the next meeting of the Fed just ahead, interest rates are drawing a lot of attention, especially with the recent upward tick in longer-term maturities. The US inflation has come down significantly since May 2023 and has hovered around 3% - 4.1% with 3.7% currently. The aggressive hikes in the past have pushed the federal fund rate up to 5.25% on the lower end, which is now substantially higher than the inflation rate. Figure 1 shows the development of both since 1994 and the recent shift. The US core PCE as an alternative measure of inflation (excluding food and energy) has also reached 3.7% for the first time since May 2021 and is an arguably more important factor for the Fed in the determination of their rate. With this positive development, it is unlikely that another hike is necessary in their November meeting. This notion is strongly supported by market participants, who see the chance for a rate increase at a probability of close to zero.

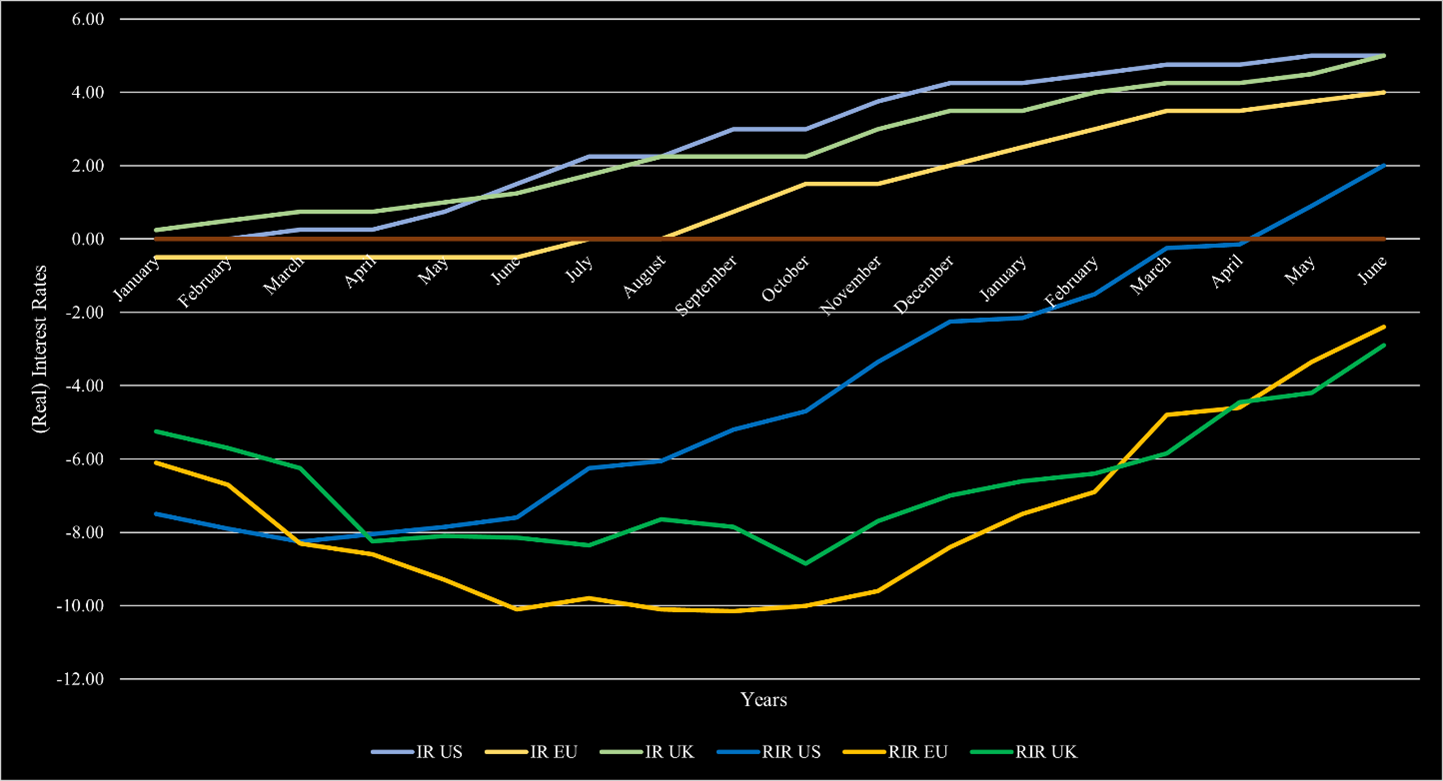

The current macroeconomic volatility has not changed. Interest rates and inflation remain elevated. At least in most markets, the inflation rate is continuously declining. In the US, inflation reached 3% and is on its way to the upper target of 2% in the short-term. Europe is following this development but still has a substantial way ahead before inflation will eventually reach those levels, as inflation remains at 6.4%. In the UK, the situation is more dire and inflation declined to 7.9% after being above 10% since August 2022. In order to bring inflation levels down, central banks have hiked substantially over the past 1.5 years. In the US, the federal fund rate is now above 5.25% with the most recent hike, which has largely been deemed unnecessary by market participants. The ECB also increased its interest rate by 25bps and is now at 4.25%. The BoE also raised its core interest rate by 25bps in their latest meeting and is now equivalent to the US’s 5.25%. The US also reached the status of positive real interest rates since the hikes started. Europe and the UK are following this trend but have not reached this territory yet. Figure 1 also shows how Europe and the UK are lacking behind the US. In the current environment, a recession is still likely. While projections have changed throughout the year, the consensus opinion remains that there will likely be a short and with a shallow to medium impact on the economy. The most notable change is that the recession expectation has pushed further and further into the future. It started with estimations that it will happen by mid-2023, then towards the end of 2023. Now, most estimates place the recession somewhen in 2024.

From a financial perspective, inflation, interest rates, and a possible recession remain the most vital topics in the short term. While inflation came down substantially in 2023, interest rate hikes have persisted thus far. In the US, the interest rate set by the Fed remains at 5% after they decided that no hike was necessary in June 2023. With the release of job data in early July, talks about further hikes have increased, as data showed that job growth has slowed. Market participants now expect further hikes in 2023. The projection from the beginning of 2023 and possible rate cuts as early as Q3 2023 seem very unlikely at this point. Figure 1 shows the expected interest rate level until 2025. Rates are expected to rise to 5.5% by the end of 2023. Based on a survey from 18 members of the FOMC, rate projections range from 5.1%-6.1% by the end of the year. In 2024 and onwards, gradual rate cuts are expected with rates around 3% by 2025. These projections are highly dependent on a positive development of inflation and job data. Recent inflation data in the US has been very promising, as inflation decreased to “only” 4%. The steep measures taken by the Fed since 2022 managed to combat inflation substantially. Excluding highly impactful developments (e.g., a steep recession or a strong escalation of war), inflation is expected to steadily decrease over the next years. By the end of 2023, inflation is expected to be around 3% ± 1% and slightly above 2% ± 2% in 2024. The expected, slowed decrease in inflation is largely attributed to the tamer measures of the Fed after their initial aggressive hikes. As these take time to become effective, the decrease should slow down. Additionally, a recession or a market correction is highly likely which may cause further issues with inflation and may slow down the effectiveness of the measure so far. Overall, the likelihood of a recession is still significantly high. The most notable differences in the expected recession compared to forecasts in early 2023 and 2022 are the recession is likely a mild one. Additionally, with the recent positive developments, a possible recession is pushed further in the future. At the end of 2022, a recession was anticipated to occur between Q3 and Q4 2023. Current forecasts expect a recession in the US in early 2024. Despite the harsh ecosystem, US equities had a great year in 2023 with a 15% return so far. On an industry level, the picture looks very different. Basically the entire gain of equities came from soaring tech stocks. On the other end of the spectrum are banking stocks, which have suffered this year, especially after the collapse of multiple large banks, such as Silicon Valley Bank and Credit Suisse. Forecasts for the value of the S&P 500 at the end of 2023 deviate substantially. In general, estimates were raised slightly compared to estimates back in 2022. On an aggregate level, investment banks expect the S&P 500 to end the year at roughly above 4,100. The highest estimates are 4,550 for the index. Contributors to these estimates are a less aggressive Fed, resilient economic growth, and the recent interest in artificial intelligence in combination with the soaring tech stocks. Bearish outlooks go as low as 3,400 points and cite a continued slide in stocks as the core reason.

The macroeconomic ecosystem continues to be the dominant topic. It was further ignited by the recent central bank decisions. While markets were rather optimistic from the US perspective, it does not apply to Europe. With the recent break from interest rate hikes by the Fed, it felt like a turnaround point. However, the Fed hinted that this was merely a break and that further hikes are not unlikely. Following the good results of the inflation data in May 2023, the Fed halted an interest rate hike for now. As of May, the inflation declined to 4%, down from 4.9% in April. These positive results mainly stem from a substantial decline in energy prices. While the development was similarly positive in Europe, inflation remains above 6%. Central bank representatives highlighted that the fight against inflation is not won yet. Hence, it was not surprising that rates were raised to 3.5%. In Switzerland, inflation has never been such a tremendous issue. Nonetheless, the Swiss National Bank also raised its rates, but only by 25bps. The most surprising move came from the UK. The BoE hiked rates to 5% through a 50bps increase. Market participants expected a 25bps hike and the BoE earned substantial critics for that move. The move likely came from the still very high inflation rate of 8.7%. Figure 1 shows the total development of interest rate hikes from the US, EU, UK, and Switzerland since the beginning of 2022. The positive news from the US also had a substantial impact on the equity market. As of the time of writing, the S&P 500 is up another 4% in June and 14% YTD. Although the Fed highlighted rate hikes might not be over, the break in hiking alongside the declining inflation is a promising sign that rates will “soon” come down and the projected recession might be averted. In particular, big tech has reacted strongly to the news, which remains the driver of the exceptional performance of the stock market this year.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |