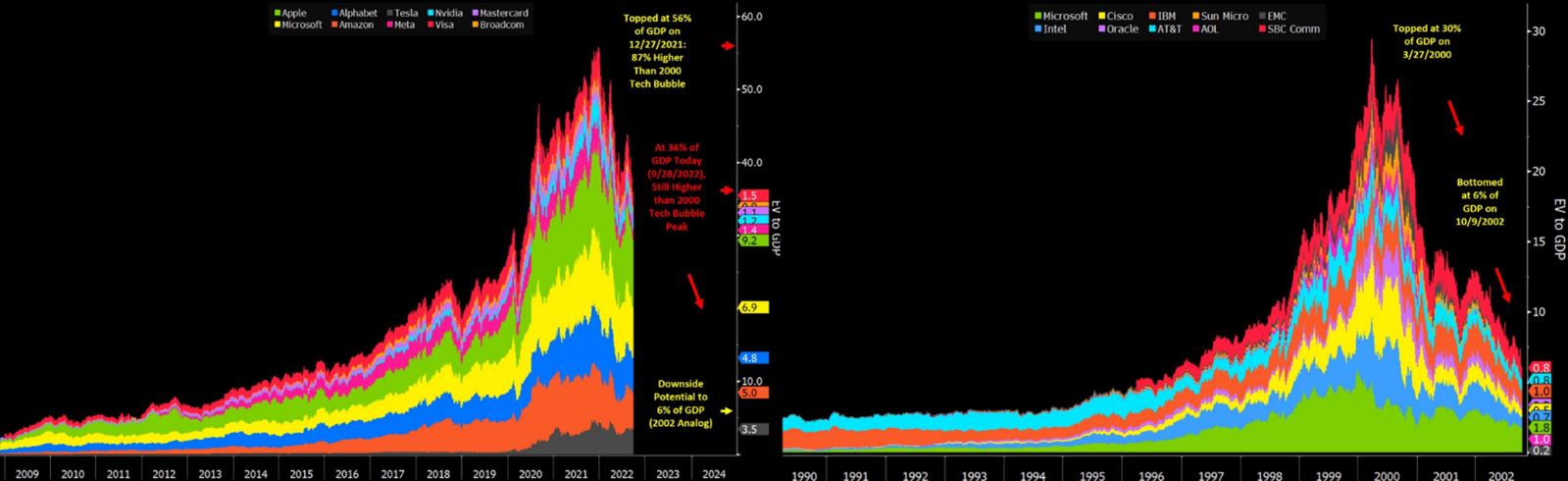

The UK’s economy continues to be under high pressure. While high inflation affects all countries, Truss’s historical tax cut and its outlined budget sent markets crashing. In particular government bonds alongside the British Pound experienced an alarming development, such that the BoE had to intervene and stabilize the economy. This had a brief stabilization effect, as the support was for a limited amount of time, as shown in Figure 1. This short support is largely due to the fact that it goes against the plan of central banks globally which try to reduce their balance sheets following the substantial interventions during Covid-19. This financial emergency led to Truss’s resignation from her position as prime minister. Her initial rival Sunak took over the office soon after and faces a tough situation ahead. Following this turmoil, markets have somewhat calmed down with Sunak’s appointment as PM and his experience in former financial positions. Meanwhile, other countries are still committed to raising interest rates. For the Fed, it is widely expected that rates will be raised by another 75bps in early November reaching 4%. With this following hike, officials say that further hikes are to be expected, although the magnitude might slow down. Further hikes are increasingly likely as the inflation rate is not really cooling down, and remains at 8.2%, down from 8.3% in the prior month. The relatively stable decline in equities is also unlikely to stop any time soon. Not only is there a constantly looming threat of a recession, but the equity market also tends to be correlated to central bank assets, as shown in Figure 2. This relationship is intuitive, as more assets or capital in the market are deployed. Furthermore, during Covid-19, much of the injected capital flew directly into stocks. With the back scaling of available capital, it is withdrawn from more risky capital, which is frequently stemming from equities. Although cryptocurrencies took a huge hit in early 2022, since July 2022, their performance is positive unlike bonds, stocks, or gold. This is a relieving sign for the industry, as cryptocurrencies tend to be strongly correlated with other asset classes at the beginning of a drawdown, but is the first asset class to recover from it. In this state, the asset class usually regains its attractive property of being non-correlated to other asset classes. Another highly intriguing development is taking place with Web3 applications. Web3 applications essentially fulfill the same role as technology companies leveraging the internet. However, unlike these technology companies, Web3 platforms are built decentral and are not maintained by a single entity. The current state of the Web3 industry strongly resembles these technology companies during the dot-com bubble. Figure 4 highlights a few key similarities. Venture investing in these types of companies also has not taken a large hit, compared to most other asset classes. This is in particular notable, as traditional venture investing took a substantial hit in 2022. Figure 5 shows the consistent decline in venture investments since Q4 2021.

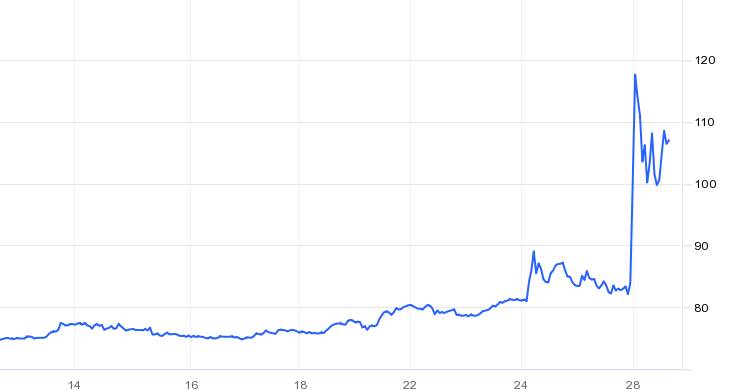

For once, inflation was not the most prominent topic over the past two weeks. Instead, it’s the UK government and its optimistic tax cut. The UK’s new prime minister Truss promised a large tax cut in her election campaign. If implemented, the tax cuts would lead to losses of around £40bn and would be the second-highest budget cut in the past 50 years. Figure 1 shows a breakdown of the largest budget adjustments over the past 50 years. This seems very optimistic given the already existing struggles with ever-soaring inflation at the 10% mark and the severe gas/oil crisis in Europe. When further details on its implementation were revealed, the UK economy faced severe issues and could only narrowly avoid a complete disaster. The British Pound almost dropped to an equivalent level to the US Dollar for short time. Especially, the bond market crashed, as the BoE initially wanted to step back its bond buying program introduced after Covid-19. Figure 2 shows the drop in the value of UK gilts with maturities exceeding 15 years. Although they have been declining since 2020, the most recent drop is substantial. Currently, UK gilts are down 54%. A complete crash could only be avoided by the BoE strongly intervening in the bond market to stabilize the situation. It is very unlikely that the BoE can afford to step back its bond buying program any time soon, as the risk of fire sales is large, especially, if market participants know that UK gilts are no longer stabilized by the BoE. With rampant inflation across the world, central banks are continuing their consistent and strong hikes to combat further rising inflation. These interest rate hikes have led to substantial bond yield increases. The G7 average 10-year bond yields have now surpassed their average yield of the past two decades, as shown in Figure 3. Given the current development, bond yields could rise to their average at the beginning of the 21st century and likely stay there for a while until inflation is under control to a large degree. While it is debatable whether central banks acted fast or not; when they started doing so, the frequency and magnitude were substantial. This is especially true for the Fed. Figure 4 shows a comparison of the speed and magnitude of the current hikes compared to other historical hike cycles. With the current expectation of two further hikes (each between 50bps and 75bps), the current cycle is not only the largest in terms of magnitude but also the fastest at any given time. Despite the strong hikes of the Fed already, inflation in the US still increased by 0.4% to 8.2%, which was higher than expected and is likely to put further pressure on the Fed. This development is likely to emphasize further rate hikes, potentially even higher than currently anticipated. Equities also continue to be under pressure. After reaching their low of the year in mid-2022, they bounced back until August 2022. Since then, they have been consistently facing losses and reached new lows in 2022. The S&P 500 index is down 25% YTD, while the tech-heavily Nasdaq is down almost 35% YTD. The outlook is certainly not great with rising interest rates and a looming global recession. Additionally, it is worrying that the Covid-19-induced bull run strongly resembles the development during the dot-com bubble. Figure 5 highlights the similarities between the two tech bull runs and potentially bubbles.

Alternative Markets Summary H1 2022

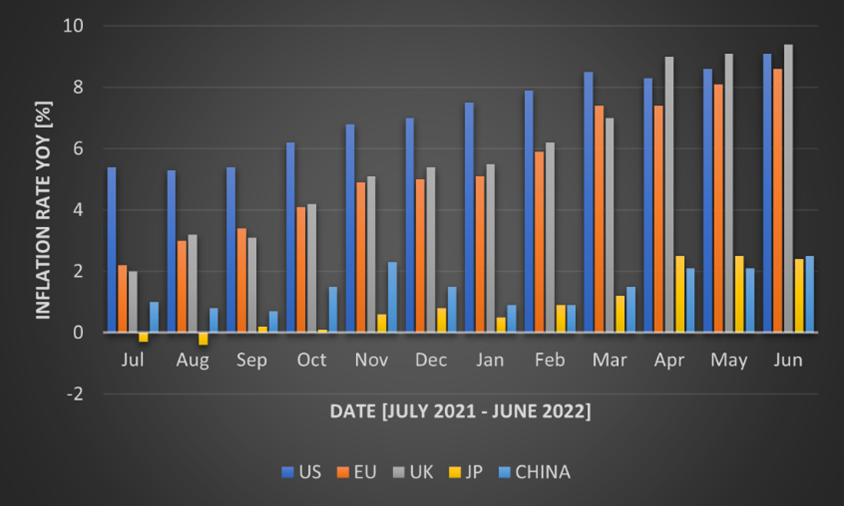

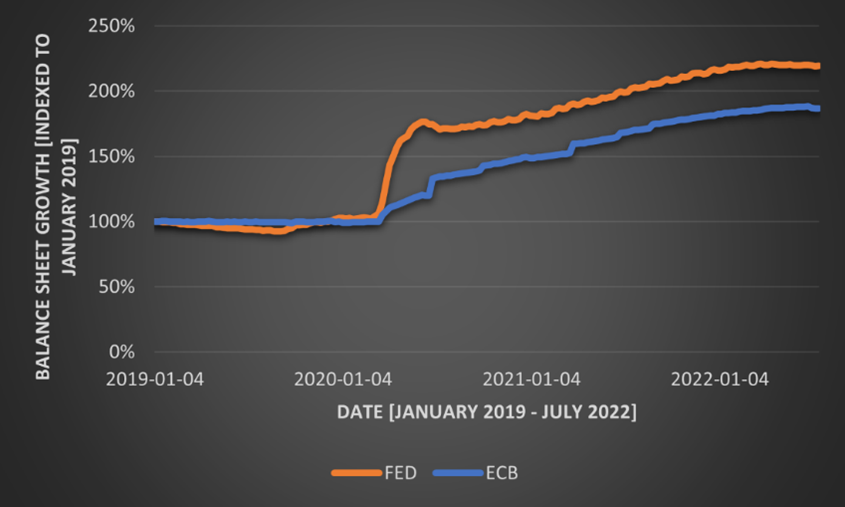

Ever since Covid-19 has subsided from the daily news, inflation has taken over. Inflation is still a major concern in the current economy. This is further exacerbated by central bank interventions that have not been fruitful yet. An additional major contributor is the ongoing war between Russia and Ukraine. As of June 2022, inflation in the US is at 9.1%, the highest it has been in the past 40 years. In the Eurozone, inflation is slightly lower at 8.6%. The UK’s inflation is even higher at 9.4%. Asian countries, such as Japan and China, managed to keep their inflation relatively low at 2.4% and 2.5%. The development of inflation over the past year is summarized in Figure 1. For Western countries, inflation has more or less continuously risen. The US started the year with inflation close to over 5%, while European countries were close to 2%. Nonetheless, Europe has caught up to the US since April, when the UK’s inflation even got higher than the US’s. A potential reason for the higher inflation in the US at the beginning of the year and back until the latter half of 2021 is the rapid and steep unconventional measures taken by the Fed. This faster intervention led to more money being in the economy earlier, which theoretically should lead to higher inflation earlier. Figure 2 shows the growth in the balance sheet indexed to January 2019. Once Covid-19 hit the economy, the US reacted a lot faster and in higher magnitudes than Europe did. Within the first months, the Fed’s balance sheet grew by almost 70%, while the ECB’s only grew by 25% in the same time frame. Since then, the two central banks acted equivalently in terms of balance sheet growth. Very recently, the central banks started to shrink their balance sheets. These measures were announced during Q2 2022 and are slowly implemented. Going forward, this balance sheet shrinking will be strengthened, which is confirmed by an announcement from the ECB recently. Nonetheless, as the graph shows, these measures barely affect the original measures taken to combat the economic consequences of Covid-19. The low inflation in China largely stems from the consequences of their zero-Covid policy. In recent months, many places have been shut down to control the spread of Covid. This led to low production levels and low demand which is reflected in the low inflation levels of the country. In the case of Japan, inflation of above 2% is significant, as the average inflation during the past three decades was only 0.3%. Its inflation largely stems from the consequences of the war and the impact it has on food and energy.

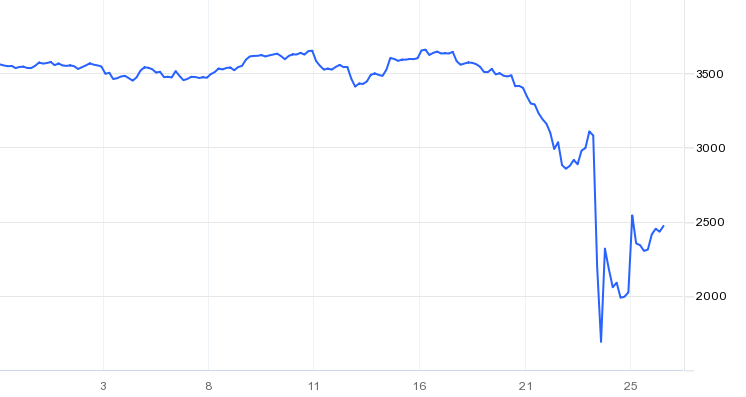

The war in the Ukraine caused by the Russian invasion is the dominant topic around the world. In particular Western states widely underestimated Putin and the likelihood of the Russian invasion. Initial rumours anticipated an invasion from Russia on Monday, 14th February 2022, as Russian troops supposedly retreated. After the invasion did not take place then, there were some signs of relief, which were short-lived. Fears started to grow when Putin acknowledged the separatists in the Eastern Ukraine, more specifically, Donetsk and Luhansk. There were crucial similarities compared to the annexation of the Crimea peninsula in 2014. While this was going on, Western countries threatened Russia with sanctions. Those did not achieve a meaningful impact, as on Thursday morning, the worst case in that situation occurred. Russia invaded the Ukraine from all angles and managed to shutdown their missile defences almost immediately. Russia conquered several parts of the Ukraine extremely quickly and found itself soon on the doors of the capitol, Kyiv. Later that day, sanctions on Russia were imposed by the US, the UK, the G7 states and most other European countries. These included freezing the assets of some of Russian elites, some banks and businesses in the respective countries. This sanctions prohibit being involved in any kind of business with those individuals, banks or businesses. The US also banned individuals from trading Russian sovereign debt. Those sanctions had little impact on the invasion of Russia. Most people hoped the sanctions would be harsher, but at that point Europe was reluctant on banning Russia from SWIFT due to their reliance on Russia’s oil and gas. The invasion truly changed into a war in the city of Kyiv and over time most countries around the world support the Ukraine with additional weapons and ammunition, while some countries even sent soldiers to help defending the country. On Monday, the SWIFT ban from some Russian banks was announced as well as the extension of listed targets and institutions whose assets are frozen. Initially, Russia’s goal was to de-weaponize the country and to replace Zelensky, the prime minister of the Ukraine, by a more pro-Russian government. Russia employed substantial propaganda and legitimized the invasion by calling the Ukraine being full of Nazis among other things. It now seems very questionable whether replacing the government was the initial target, as it feels much more like a full annexation. This puts in particular the Baltic states into a state of alert, as if Putin’s goal to recreate the former Soviet Union, then they are likely the next target. This also explains the harsh threats from Russia when discussions were held whether Finland should become a NATO state. Further unpleasant developments are that China can be considered neutral towards Russia’s actions, as they first supported the Russian invasion given the reasons from Russia. However, they also followed through on Zelensky’s call to talk to Putin on possibilities to resolve this war. After an initial discussion between the Ukraine and Russia was denied by the Ukraine, it seems to be likely that Putin and Zelensky agreed to a meeting. This comes after Russia’s threat of using nuclear warheads. Unsurprisingly, markets reacted with tremendous volatility over the past two weeks. The sanctions on Russia had a detrimental effect on Russia’s economy. The Russian Rubel collapsed by 30% after Western countries announced the SWIFT ban for some Russian banks, after the Rubel has already lost substantially in value since the start of the invasion, as shown in Figure 1. Russia’s equity market also took a huge hit. On the day of the invasion, the MOEX Russia Index dropped by almost 50% from 3,200 down to 1,700. Despite its recovery, it is questionable how Russian equities will perform in the short-term future, as further sanctions are likely and make doing business outside Russia very difficult.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |