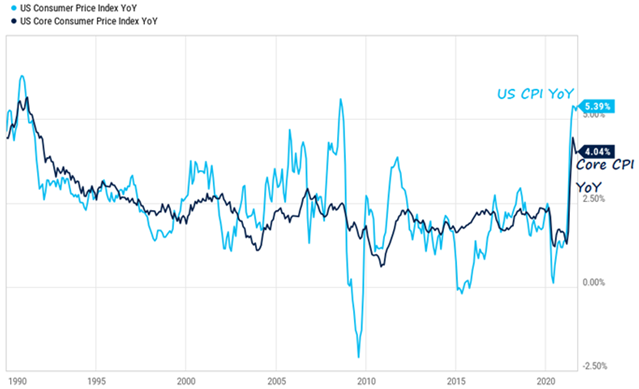

2023 followed the core theme of 2022 with a key focus on inflation and interest rates. At the beginning of 2023, inflation was a huge concern, due to its high level. In the US, inflation was at 6.5% and already declined substantially from its peak in June 2022 at 9.1%. This trend continued in 2023 until it reached its bottom in June 2023 at 3%. Since then, US inflation remained steady between 3% and 4%. The EU and the UK saw a very similar development of inflation throughout 2022. Their respective inflation started at around 5.5% in January 2022 and rose to 10.5% by the end of 2022. As soon as 2023 started, inflation in the EU started to decline and eventually declined to as low as 3.1% in November 2023. Despite this promising development, inflation began to increase again to 3.4% in December 2023. While the UK’s inflation development was almost equivalent to the EU’s in 2022, this changed in 2023. Inflation in the UK remained above 10% until April 2023, at which point inflation was at 10% or higher for almost an entire year. Nonetheless, UK inflation also came down later in 2023 and reached the 4% mark at the end of December 2023. Based on the overall relatively similar development of inflation around the world, it is likely that inflation will stay at elevated levels in the short term. Another key reason for relatively stale inflation is that central banks stopped hiking their interest rate for a while now in 2023. Figure 1 summarizes the development of inflation in the US, EU, and the UK.

With the soaring inflation in 2021 and afterward, central banks had to react. Financial markets enjoyed rates close to zero, if not negative, for a long time. As a response, central banks started raising their interest rates. The Bank of England was the first to raise its interest rates in December 2021. The Fed followed in March 2022 and hiked its rate in every meeting and by a higher amount on average than the BoE or the ECB. The BoE did so too, but did smaller hikes on average. The ECB followed in June 2022, but they did not hike at every meeting. At the start of 2023, the interest rate in the US was already at 4.25% compared to 3.5% in the UK and 2.5% in the EU. Consequentially, the ECB hiked more in 2023 but did not reach the same heights as in the US or UK, which are currently at 5.25%, while the ECB’s interest rate remains at 4.5%. With interest rates now higher than inflation rates in each of those economies, most market participants expect interest rate cuts in 2024, especially due to an elevated possibility of a recession ahead.

Alternative Markets Outlook 2022

2021 was firmly in the grasp of Covid-19 through the Delta and Omicron strain. Although Covid-19 was managed solidly, the imposed restrictions and the economic interventions have severely impacted the economy and society. Not only has inflation skyrocketed but it is also likely to persist for quite some time. In January 2021, the US CPI was at 1.4% and rose to 6.8% in November 2021. In Europe, the situation looks similar, although the initial surge started earlier in the US and currently Europe’s inflation is lower with 4.9% in November 2021. In 2022, inflation will prevail with even higher levels in early 2022 with a realistic chance to subside towards the latter part of 2022. This rather grim outlook is largely in line with the observation during 2021, when inflation targets were mostly too low and the estimated time period were too short. The US will probably experience slightly higher levels, due to the larger extent of money printing to fight Covid-19 originally. Central bank intervention will be reduced to normal levels in the latter part of 2022. It has been already announced that they will scale back their asset buying programs but not entirely. Depending on how Covid-19 is evolving, it seems reasonable that towards the end of 2022, these programs will be discontinued. Aside from these monetary interventions, there were also substantial fiscal interventions, as shown in Figure 1. Figure 1 depicts the US national debt and the increase of additional trillion of debt. Since Covid-19 emerged, six additional trillions were spent to fight the immediate impact. In particular, the speed at which the money was spent is remarkable. While it took between 30 and 300 days for an additional trillion during Covid-19, it took between 170 and 320 days during the global financial crisis in 2008. The measure undertaken to fight Covid-19 are massive but they have helped the economy to bounce back. Among others, the development of the employment is largely desirable. For example, in the US, the unemployment rate was reduced to 4.2% from its peak of more than 14% in 2020. Equity markets, which have contributed in a major fashion to the overall success of 2021, will be largely impacted by Covid-19 in 2022. This was once again observable in November 2021 when Omicron emerged. Assuming a positive development, it is likely that equity markets will keep rising, although at a normal pace below unlike 2020 and 2021. Figure 2 and 3 show the S&P 500 and the Euronext 100 indices over the past two years. Since January 2020, the S&P 500 gained 47.5%, while the Euronext 100 gained 18.9%. The gains since their bottom in March 2020 are 118.4% for the S&P 500 and 86.0% for the Euronext 100. One potential reason for the strong growth in 2020 and 2021 may be due to expected inflation ahead, which is compensated by higher nominal gains. This effect is likely to fade given the enormous growth numbers in 2021 which have given rise to doubts about the sustainability of these profits alongside fears of another financial bubble. This is in particular true for industries that have benefited from Covid-19, such as technology. One example of seemingly unhealthy gain is Tesla, which is up more than 1,000% since Covid-19 emerged. The companies benefiting from Covid-19 should be viewed with caution, while companies that were negatively affected by Covid-19 certainly involve less risk. A negative development with the handling of Covid-19 could turn the situation upside down again and trigger similar effects as in March 2020. This may occur, for example, if a new strain emerges with a substantially increased fatality rate, is spread relatively easily and vaccinations are of only mediocre effectiveness against the new strain. Yet, this scenario is rather unlikely given that with each wave, the number of infections remains at a relatively similar level, while hospitalizations and fatalities decline. Furthermore, virus strains that spread more easily, such as Omicron, frequently are less deadly. These two observations favour the good scenario going forward. In an environment of high volatility and many opportunities, alternative assets are well positioned. Figure 4 highlights the volatility in the market measured by the VIX. Since the occurrence of Covid-19, the volatility in markets has never reached levels prior to Covid-19, although there has been a massive improvement. From the peak in March 2020 and a level of more than 80, markets have stabilized between 15 and 25 in quiet times with occasional spikes. With regards to alternative assets, 2020 and 2021 were highly beneficial for several reasons. Firstly, in crises, actively managed vehicles are of increased interest as they try to mitigate the negative impact of the crisis. Secondly, due to the nature of being a healthcare crisis, this brings many opportunities with it. Thirdly, the substantial uncertainty in markets also favour alternative assets, as for example, private equity funds are less sensitive to significant short-term volatility. 2021 was especially profitable for the private equity and hedge fund industry, which make up the largest part of alternative assets. In the following sections, hedge funds, private equity, private debt and crypto assets are discussed in a more detailed fashion.

The most noteworthy event in September 2021 was probably the apparent collapse of Evergrande, one of the largest real estate companies in China, whose status is currently unknown. On Thursday, 16th September 2021, Evergrande issued a statement that it will not be able to repay the outstanding interest payments that day. Following this announcement, the financial market was in substantial stress. Equity markets all around the world lost a few percentage points and volatility spiked. Bond trading was under pressure as well, as Evergrande’s bonds were downgraded and frozen from trading. It sometimes was already referred to the next “Lehman Brothers” case. The volatility the stock has seen since is tremendous, as it lost nearly 80% in the first few days after the announcement. It seemed as though the situation had stabilized, but since not all due payments were paid on Friday, 24th September 2021, the status is unknown. If nothing else happens, which is highly unlikely, the company would enter a grace period following bankruptcy. There are three critical features involved in Evergrande. Firstly, China and Chinese people are heavily engaged with the company, as the company has sold many buildings already without having built them yet. A default would cause huge issues for the affected people. Secondly, many companies are frequently doing business with Evergrande, in particular construction, design and other suppliers, could also face bankruptcy alongside Evergrande. Lastly, the collapse of Evergrande would pose a substantial risk to the financial system of China. The latter one is in particular difficult, as the company has outstanding debt at more than 250 banks, which could put additional pressure on China’s ability to offer cheap debt, which is necessary to maintain growth level. Moreover, it does not make a China a more appealing place to invest for foreign investors, which were already on the decline since the recent developments

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |