alternative markets update - mid january 2022 & 2022 Crypto Predictions by Paul Veradittakit13/1/2022

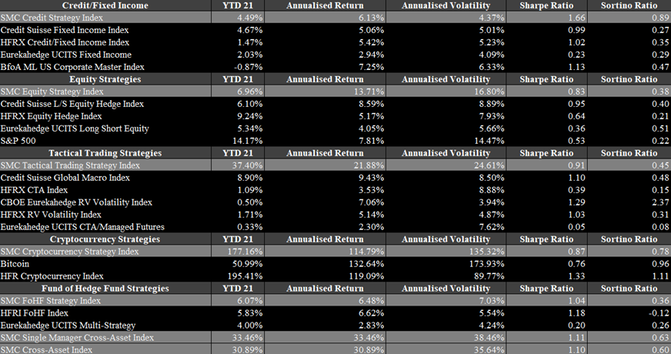

Hedge funds have experienced a great third quarter and continue to do well in October 2021. Partially due to the surge in volatility, the hedge fund industry is close to reach a milestone of $4tn in AuM. Nevertheless, the strategy of hedge funds is of utmost importance when determining how well a hedge fund is doing. This is in particular true for 2021. Crypto and equity hedge funds tend to profit the most from the current market ecosystem, as their asset class is surging at a rapid pace. Global macro and fixed income-based strategies have a more challenging ecosystem. Figures 1 to 6 show the returns as of Q3 2021 of the different SMC Strategy Indices in comparison to other relevant benchmarks for the specific strategy. Cryptocurrency strategies unsurprisingly did the best this year with the average strategy being up 177%. All strategies in that area cover the best performing strategies of the year with Token Liquid and Token being the best among them with a performance of 316% and 260%. The SMC Equity Strategy Index achieved a lower return than some of its benchmarks in 2021 with 7% as of Q3 2021. The best performing equity strategy is Equities US Activist Event Driven which is 27% up in 2021. With regards to the less beneficial ecosystems for fixed income and global macro related strategies, the SMC Strategy Indices did well. The SMC Credit Strategy Index is up 4.49% an outperforms almost all benchmarks shown in Figure 2. The situation is even better for the SMC Global Macro Strategy Index that achieved a YTD of 37.40%, thereby outperforming any benchmark by a lot as shown in Figure 4.

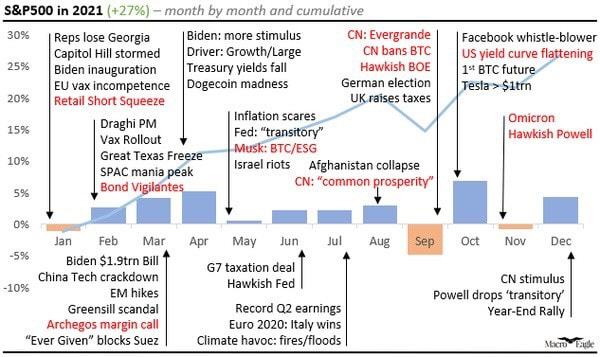

The most noteworthy event in September 2021 was probably the apparent collapse of Evergrande, one of the largest real estate companies in China, whose status is currently unknown. On Thursday, 16th September 2021, Evergrande issued a statement that it will not be able to repay the outstanding interest payments that day. Following this announcement, the financial market was in substantial stress. Equity markets all around the world lost a few percentage points and volatility spiked. Bond trading was under pressure as well, as Evergrande’s bonds were downgraded and frozen from trading. It sometimes was already referred to the next “Lehman Brothers” case. The volatility the stock has seen since is tremendous, as it lost nearly 80% in the first few days after the announcement. It seemed as though the situation had stabilized, but since not all due payments were paid on Friday, 24th September 2021, the status is unknown. If nothing else happens, which is highly unlikely, the company would enter a grace period following bankruptcy. There are three critical features involved in Evergrande. Firstly, China and Chinese people are heavily engaged with the company, as the company has sold many buildings already without having built them yet. A default would cause huge issues for the affected people. Secondly, many companies are frequently doing business with Evergrande, in particular construction, design and other suppliers, could also face bankruptcy alongside Evergrande. Lastly, the collapse of Evergrande would pose a substantial risk to the financial system of China. The latter one is in particular difficult, as the company has outstanding debt at more than 250 banks, which could put additional pressure on China’s ability to offer cheap debt, which is necessary to maintain growth level. Moreover, it does not make a China a more appealing place to invest for foreign investors, which were already on the decline since the recent developments

The macroeconomic environment will largely drive the market in H2 2021, which itself is based on significant degree how Covid-19 will evolve in the near future. With regards to the pandemic, the key questions are how the number of vaccinations evolve going forward, in particular as developed economies no longer have shortages of vaccines, but rather a declining number of people that want to get vaccinated. A crucial point is whether herd immunity can be achieved, either by being vaccinated or having had the virus. Another important point is how long the vaccine will last, as the cases of vaccinated people contracting the virus rises. Luckily, the symptoms seem to be minor. Probably even more important is whether new strains of the virus emerge that completely bypass vaccinations and essentially setting the world back to March 2020. The latter scenario seems less likely but should be considered to some degree. In a non-negative scenario, US inflation is likely to drop towards the end of the year with expectations around 3%. For the next years, it is expected that US inflation will remain between 2% and 3%, following the change in the FED’s inflation target of being 2% in the long-term instead of capping inflation at 2%. Thus, it is unlikely that inflation will drop below 2% for quite some time. In the EU, the inflation outlook is lower compared to the US, as the ECB expects inflation to rise to around 2.6% in Q4 2021. In 2022 and 2023, inflation is expected to remain around 1.5%. Furthermore, the FED and ECB also hinted at possibly putting more emphasis on employment instead of inflation going forward. This suggests gold being well positioned in the current market. As of July 2021, gold is almost back at its average in 2021 of $1800 per ounce. Despite being at a relatively high level historically, gold seems attractive with surging inflation and short-term interest rates being very close to 0%. Yet gold’s record high of more than $2000 per ounce lies back almost a year, at a point in which inflation was at 1% and not a concern for many. Since May 2021, inflows in gold ETFs are positive again albeit a bit sluggish. This is remarkable as previously, there were mostly only net outflows. Currently, the global gold AuM is at $214bn. Equities, in particular in the US, have experienced a great 2021, as shown in Figure 1. The S&P 500 is trading very close to its record high of around 4,450. During 2021, expectations for the S&P 500 level were adjusted multiple times. At the end of 2020, when the S&P 500 was 3,700, moderate expectations were around 3,900, while optimistic scenarios targeted 4,300. Yet, all those expectations were already surpassed in the low-interest rate environment, monetary stimulus and increased corporate earnings due to the recovery of the economy. Goldman Sachs has updated its target for the S&P 500 to 4,700 at the end of 2021. Contrarily, Chinese tech companies have suffered in July with the worst month since the financial crisis in 2008. Investors feared the crackdown of Chinese regulators on tech companies. Figure 2 shows valuations of Chinese companies listed in Hong Kong and in the US. Not only, are Chinese tech companies strongly undervalued compared to US tech stocks. Furthermore, Chinese tech companies listed in the US are even stronger undervalued, as very few even reach a multiple of 5, as shown in Figure 2.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |