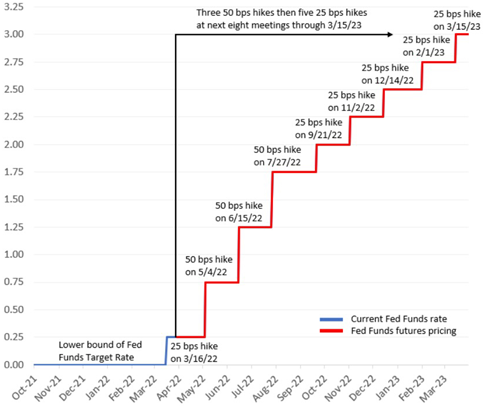

Aside from the continuous news about the ongoing war between Russia and the Ukraine, macro events are increasing after they have been halted when the war started. Central banks will increase the interest rates gradually over the year to combat the steadily rising inflation. After Powell announced at the beginning of the year that there will be many, but small, interest rate hikes in 2022, equity markets lost substantially. The first interest rate hike was expected early on but was postponed and again when the war started. Even though the war is ongoing, in mid-March 2022, the Fed announced the first 25bps hike. In a statement a week later, Powell showed a more aggressive stance to get inflation under control by outlining the plan of six further 25bps hikes in 2022, which will take place after each meeting. For May, he outlined that there is a high chance that the hike may even be 50bps. Figure 1 summarizes the expectations of the interest hikes in the coming year. These planned hikes pose a major treat for an inversion of the yield curve, as the spread between 2y and 10y notes dropped to only 13bps as of last week. On Monday, the 28th March 2022, the yield curve inverted as the yield on the 5-year notes rose above the yield of the 30-year note. In all prior Fed tightening cycles since 2000, the yield curve inverted. This is particularly relevant, as this was just the first of planned seven hikes this year and the decline in the spread between short- and long-term rates has rarely been that quick. As a sign of a recession, it remains to be seen whether this scenario unfolds against Powell’s view of a flourishing economy, due to increased interest rates. Figure 2 shows the previous yield curve inversions since 2000. Increased interest rates also increase the attractivity of bonds, as they will generate returns again. Since Covid-19 when interest rates were basically zero at all times, attractivity of bonds substantially decreased which led to soaring equity market as bonds were no longer viable alternatives. It also fuelled the commodity rally, as bonds did not provide an alternative to manage inflation concerns. This led to many commodities reaching all-time highs at some points since Covid-19 emerged. The interventions of central banks to mitigate the economic effects of Covid-19 have caused an extreme situation and most macro variables are at record levels, or at least at a record level of a long timespan, as shown in Figure 3. Inflation is the major concern for central banks in 2022, as, for example, inflation reached 7.9% in the US in February. Europe is not doing much better, especially given the context of steep increases months later than in the US. While the ECB is holding interest rates for at least until the latter half of 2022, the BoE has increased interest rates three times already in 2022. The latest hike came in mid-March 2022 and was the third consecutive meeting in which interest rates were raised by 25bps each which results in rates of 0.75%. This also makes the BoE the first central bank to set its interest rate to pre-Covid levels. Now, the tone in terms of a tightening policy has been reduced to balance the impact of inflation and the economy, especially because of the soaring gas and oil prices from the Russia-Ukraine conflict. Figure 4 shows a summary of the CPIs of the UK over the past year and emphasizes the steep increase in most measures. The BoE also adjusted its forecast upwards to an average inflation of 8% in Q2 2022.

Comments are closed.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |