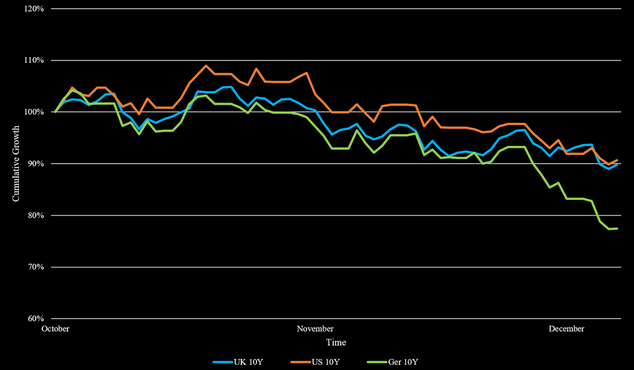

The month of November has been quite successful for equities and bonds alike. With the stabilizing macroeconomic landscape, markets have adjusted to the current state with high rates and moderate to high, but decreasing, inflation. In the past month, there were promising signs that no more hikes are necessary to combat inflation. A notable percentage of market participants is even optimistic about rate cuts soon. While US inflation has gone down substantially already in summer, European countries are following and are on their way to similar levels as the US. Unsurprisingly, this led to a more positive view on longer-term rates. This was evident in falling yields for longer-term bonds. US and UK 10-year bonds’ yield decreased by around 10% since October, while German 10-year bonds decreased by almost 25%. Figure 1 summarizes the development of 10-year yields from October in the previously mentioned countries.

Comments are closed.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |