The stillstand around the US debt ceiling was finally resolved. While it eased some of the short-term pressure on markets, it is unlikely that the general pressure will be reduced. Since the resolution of the conflict, equities and treasury yields have risen slightly. This development likely has no beneficial implications in the medium and long-term, as it was very unlikely that US politicians would have allowed the US to reach its debt ceiling. They mostly used the discussion to push their political agendas. There is also positive news on the inflation topic. In the US, inflation is at a two-year minimum with “only” 4% and decreased to 6.1% in the EU. While it is still well above the target threshold of 2%, it is a relieving and consistent development. Since a couple of months after central banks started hiking, inflation has decreased steadily albeit with some exceptions when goods affected by war became sparse. In the US, a hike pause or even a hike stop seem to be more realistic. Similar developments can be expected in the EU, but it will likely happen at a later date. With the positive news recently, the S&P 500 also entered a new bull market. From its low in October 2022, the index gained 23.8%. Figure 1 highlights the drawdown of the index in early 2022 and its impressive recovery since then. Since the beginning of June 2023, the crypto markets in the US was rattled by the SEC. The tension between major cryptocurrency exchanges and the SEC is continuing to grow. The SEC sued Binance and Coinbase for different reasons. Binance was sued, as Binance US claimed to be an independent platform for US investors and the SEC argues that the CEO of Binance, Zhao, still controls the trading platform. The SEC sued Coinbase’s trading platform as it allegedly operates an unregistered national securities exchange. Within the Binance lawsuit, the SEC also argues that tokens, such as Solana, Polygon, and Cardano are securities. The latter two claims have huge implications for the crypto market in the US. The space is still insufficiently regulated and most companies have been pushing for clear legislation for years, in particular as digital assets have been removed from the latest hedge fund regulation update. These lawsuits and the conflict between large crypto companies and regulators are likely to spark further discussions on the topic of crypto regulation.

Inflation remains a major concern and continues to exert pressure on markets. At least inflation is declining in most economies. In the US, inflation is declining since July 2022 due to the most aggressive measures taken by the Fed in comparison to other economies. Inflation fell from over 9% to now below 5%. The EU’s inflation kept rising until September 2022 when it surpassed the 11% mark. The more hesitant central bank interventions and higher exposure to the war led to a substantially slower decrease. As of April 2023, inflation still remains slightly above 8%. Toward the end of 2022, the UK behaved similarly to the EU, but could not maintain this trend. As of March, inflation in the UK remained above 10%. The continued struggle of the UK – in comparison to the EU – is largely attributable to a combination of its higher food price inflation, high reliability on gas, and worker shortages as well as wage rises. The latest data revealed that the UK could substantially reduce its inflation in April to below 9%. China and Switzerland were able to keep their inflation below 4% throughout this period and have achieved decreasing inflation similar to the previously discussed economies, albeit for different reasons. Japan followed this development but saw a spike in inflation in April 2023, which stems from a surge in food prices. Figure 1 summarizes the inflation rate development from the beginning of 2022. Figure 2 shows the corresponding interest rate measures the various central banks undertook. The Fed took the most aggressive measures with the current range being between 5% and 5.25%. Market participants widely expected rate hikes to stop earlier in 2023, and it seems now that during the June meeting, there will be a break. However, officials stated that the fight against inflation is not over, and further hikes are still reasonably likely. This dampened the optimism of market participants, especially considering views at the beginning of the year with fewer increases and possible cuts as early as autumn. Such a development seems highly unlikely at this stage. The BoE followed the Fed’s development most closely. Unfortunately, it did not achieve the same results, as the substantial discrepancy in inflation data shows. The ECB took almost half a year longer to implement such measures. As of May 2023, central bank rates in the EU are still 1.25% lower than compared to the US. It is also reasonable to assume that the ECB will continue hiking to offset its currently substantially higher inflation. This can be attributed to the later reaction of the ECB in comparison to the Fed. Switzerland, which had fewer problems with inflation, required less severe interventions. In total, the SNB increased its core interest rate by 2.25% since May 2022. In contrast to other Western economies, its core interest rate sits at a moderate 1.5%. Asian countries, such as China and Japan have struggled little with inflation and needed no or only minor central bank interventions. Nonetheless, the countries still did not go through the aftermath of Covid unscathed.

Despite the recent bank crashes and the increased recession fears they caused, markets have stabilized and performed well in the latter half of March and the beginning of April. Over the past months, the S&P 500 gained almost 7% and holds its position above 4,100. Similar developments occurred for gold and oil prices, with gold being up nearly 7% too, and oil close to 8%. While the gains from the equity markets can be largely attributed to a sign of relief that the banking crisis did not amount to a full crisis and a real possibility of the rate hikes stopping. The strong performance of gold can be largely attributed to the same factors. Within the recent bull run, gold reclaimed the $2000 per ounce mark. While oil plummeted for most of the year, its increase is caused by OPEC+’s last meeting when they announced a sharp production cut.

The crypto industry has been quiet in 2023 thus far. Despite the banking crisis and recession fears, the industry has done. Bitcoin (BTC), the most important coin is almost 80% in 2023 as of the time of writing. While Ethereum (ETH) has been less successful, it is still up 60%. Solana (SOL), a cryptocurrency that has been heralded as Ethereum-killer in 2021 completely collapsed in 2022 when it turned out the chain has substantial security issues. To address these issues the coin has been shut down multiple times which made investors lose confidence in the chain. On 12th April 2023, ETH will implement its Shanghai upgrade which led cryptos rally. The Shanghai upgrade will allow validators and stakers to withdraw their assets from the Beacon chain (the original sub-chain which allowed for the proof-of-stake consensus algorithm), which has not been possible since 2020. In total, more than 16 million ETH were locked on the Beacon chain so far. Although it is another upgrade to the chain, many see this update as “price”-neutral. While it makes staking and validating more attractive now, a lot of capital was locked and will be free for the first time in more than two years. However, most people think that not much will be withdrawn, given the dominance of ETH in DeFi and the relatively high staking yield. Additionally, ETH was worth a lot more and people will want to chase similar highs. While most cryptos rallied ahead of the upgrade, ETH was outpaced by both BTC and SOL. BTC additionally surpassed the $30k mark for the first time in a year ahead of the upgrade. Figure 1 shows the YTD of the three coins mentioned above.

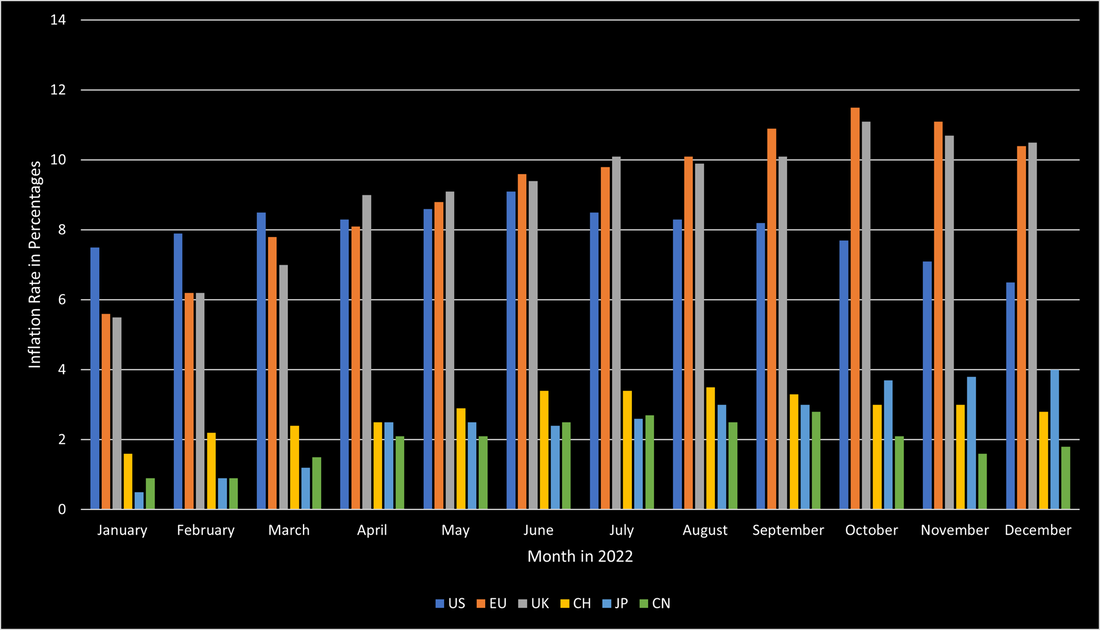

2022 was a year that tested the worldwide economy. The highest inflation in 40 years, unprecedented interest rate hikes, and the invasion of Russia into Ukraine were only some contributors to the hugely difficult year of 2022. In the US, inflation started soaring during 2021 and peaked in the summer of 2022 at 9.1%. Thanks to the central bank’s quick response, inflation has since continuously slowed down and is currently at 6.5%. Europe had significantly more issues handling the inflation crisis. The EU started the year at an inflation rate of slightly above 5.5% and it continued to soar until October 2022 when it reached its peak at 11.5%. The UK was similarly affected, despite the BoE being the fastest-acting central bank to raise interest rates. However, its inflation behaved like the EU’s and soared to its peak at 11.1% in October 2022. Both economies have not been able to reduce inflation below 10% so far. In contrast to the US, European countries were much more affected by the direct impact of the war between Russia and Ukraine. Soaring energy and food prices, for both of which Russia and Ukraine are crucial suppliers, were the main constituents causing the high inflation. Additionally, the ECB did not enjoy as much freedom as the Fed had when raising interest rates. This is in large part due to the high indebtedness of certain European countries that would have gone bankrupt if interest rates would have been raised as much as the US did. Other countries, such as Switzerland, Japan, and China stand out in this discussion, as those countries managed to keep their inflation relatively low. Switzerland managed to avoid such high inflation due to its strong currency, and a limited dependency on fossil fuels. Japan avoided high inflation through the continued quantitative easing by the BoJ. However, in contrast to the other countries, Japan’s inflation is still soaring and poses substantial issues to the country. China avoided high inflation through its rigorous Covid policies and its limited governmental support when Covid emerged. The source of this soaring inflation is a combination of the war but is largely based on unprecedented central bank intervention to save the economy during the early Covid days when large parts of the economy were completely unable to function. Figure 1 shows the inflation levels of the previously mentioned countries during 2022.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |