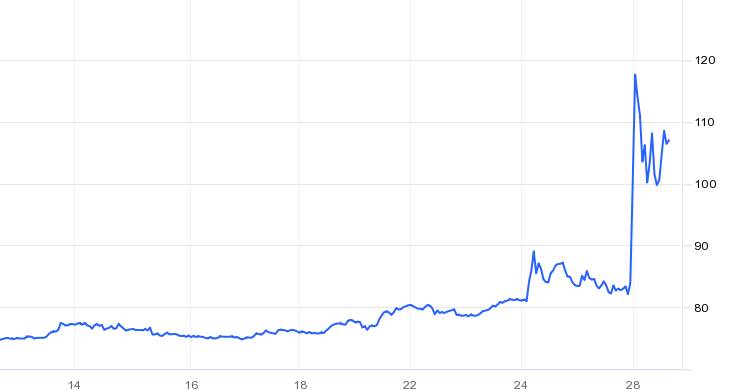

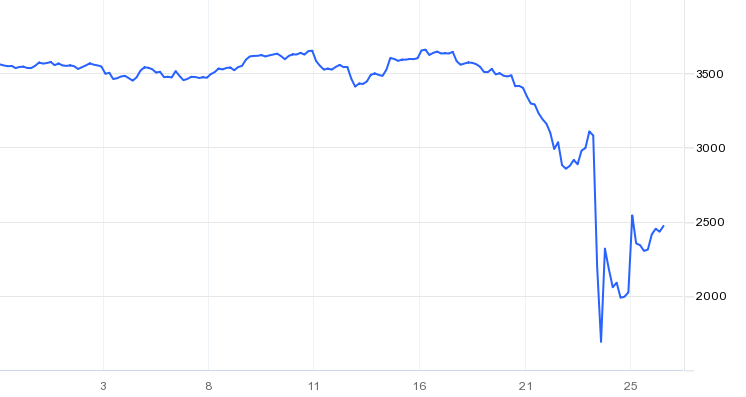

The war in the Ukraine caused by the Russian invasion is the dominant topic around the world. In particular Western states widely underestimated Putin and the likelihood of the Russian invasion. Initial rumours anticipated an invasion from Russia on Monday, 14th February 2022, as Russian troops supposedly retreated. After the invasion did not take place then, there were some signs of relief, which were short-lived. Fears started to grow when Putin acknowledged the separatists in the Eastern Ukraine, more specifically, Donetsk and Luhansk. There were crucial similarities compared to the annexation of the Crimea peninsula in 2014. While this was going on, Western countries threatened Russia with sanctions. Those did not achieve a meaningful impact, as on Thursday morning, the worst case in that situation occurred. Russia invaded the Ukraine from all angles and managed to shutdown their missile defences almost immediately. Russia conquered several parts of the Ukraine extremely quickly and found itself soon on the doors of the capitol, Kyiv. Later that day, sanctions on Russia were imposed by the US, the UK, the G7 states and most other European countries. These included freezing the assets of some of Russian elites, some banks and businesses in the respective countries. This sanctions prohibit being involved in any kind of business with those individuals, banks or businesses. The US also banned individuals from trading Russian sovereign debt. Those sanctions had little impact on the invasion of Russia. Most people hoped the sanctions would be harsher, but at that point Europe was reluctant on banning Russia from SWIFT due to their reliance on Russia’s oil and gas. The invasion truly changed into a war in the city of Kyiv and over time most countries around the world support the Ukraine with additional weapons and ammunition, while some countries even sent soldiers to help defending the country. On Monday, the SWIFT ban from some Russian banks was announced as well as the extension of listed targets and institutions whose assets are frozen. Initially, Russia’s goal was to de-weaponize the country and to replace Zelensky, the prime minister of the Ukraine, by a more pro-Russian government. Russia employed substantial propaganda and legitimized the invasion by calling the Ukraine being full of Nazis among other things. It now seems very questionable whether replacing the government was the initial target, as it feels much more like a full annexation. This puts in particular the Baltic states into a state of alert, as if Putin’s goal to recreate the former Soviet Union, then they are likely the next target. This also explains the harsh threats from Russia when discussions were held whether Finland should become a NATO state. Further unpleasant developments are that China can be considered neutral towards Russia’s actions, as they first supported the Russian invasion given the reasons from Russia. However, they also followed through on Zelensky’s call to talk to Putin on possibilities to resolve this war. After an initial discussion between the Ukraine and Russia was denied by the Ukraine, it seems to be likely that Putin and Zelensky agreed to a meeting. This comes after Russia’s threat of using nuclear warheads. Unsurprisingly, markets reacted with tremendous volatility over the past two weeks. The sanctions on Russia had a detrimental effect on Russia’s economy. The Russian Rubel collapsed by 30% after Western countries announced the SWIFT ban for some Russian banks, after the Rubel has already lost substantially in value since the start of the invasion, as shown in Figure 1. Russia’s equity market also took a huge hit. On the day of the invasion, the MOEX Russia Index dropped by almost 50% from 3,200 down to 1,700. Despite its recovery, it is questionable how Russian equities will perform in the short-term future, as further sanctions are likely and make doing business outside Russia very difficult.

Hedge Funds

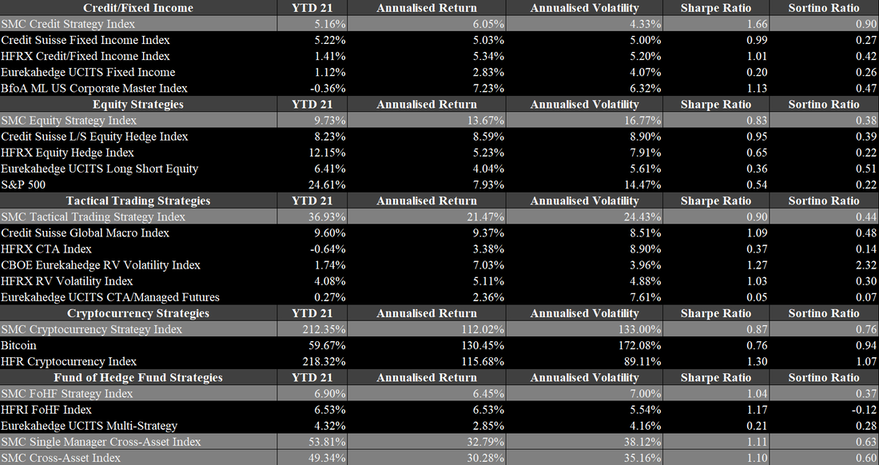

Hedge funds had a great 2021 and managed to set a record high in its AuM. As of the third quarter in 2021, the AuM of the industry is expected to be between $4.3tn and $4.6tn depending on the sources. According to BarclayHedge, the industry’s AuM just surpassed the $4.5tn mark at the end of the third quarter. This is a steep increase from just $3.8tn in 2020, as shown in Figure 6. This is a gain of more than 18% in less than a year. It is expected that the number will rise slightly, once the Q4 2021 numbers are out, as October and November 2021 were rather positive. Nonetheless, December 2021 will have dampened the results of Q4 2021. Generally, the industry has gained substantially over the past ten years, despite a rather inferior view from market participants during most of that period. The AuM soared thanks to two reasons. Firstly, the industry saw substantial capital net inflows. During the first three quarters, the industry received $41bn in fresh capital after having received another $19bn in the second half of 2020. Since then, the industry saw net inflows in every quarter, which is stark break from previous years when the industry experienced net outflows in most quarters. In Q4 2021, net inflows rose to $81bn in 2021, according to Eurekahedge. Figure 7 also shows the severe initial impact of Covid-19 in 2020, when accounting for the significantly positive inflows in the latter half of the year. The second reason for the steep increase in AuM is due to the performance of the hedge fund industry in 2021. Hedge funds in 2021 returned slightly more than 10%, making it the third best year in history after 2020 and 2009 according to HFR. This is remarkable, as the year has not been easy with the constant uncertainty and high volatility in the market. In particular event-driven, equity and commodity strategies have performed very well and the high beta strategies within their respective sector. Figure 8 summarizes the performances of several strategies during 2021 by Eurekahedge. Distressed debt and event-driven strategies performed best with barely any negative performances during the year. Macro and fixed income strategies struggled the most throughout the year, due to the harsh economic conditions. When looking at the highlighted percentiles, it is evident that the high volatility in the market also caused high volatility in hedge fund returns, independent of the strategy. This is most relevant for long short equity strategies whose returns vary between +30% (upper percentile) and -10% (lower percentile) in 2021. Figures 9 to 13 highlight the SMC Strategy Indices in 2021 compared to their benchmarks. The SMC Credit Strategy Index gained slightly more than 5% in 2021, although the variation across strategies is substantial. Two strategies, Trade Finance Crypto and European High Yield L/S Credit did very well in the economic environment, as they reached returns above 12% and 19% in 2021. The Trade Finance Strategy is in particular remarkable, as the strategy has not experienced a negative month since its inception in 2017. The SMC Equity Strategy Index gained closely less than 10%, which is around as much as the average equity strategy in 2021. Within the sector, there was also considerable volatility, due to the sub-strategies. Unsurprisingly, the Equities US Activist Event-Driven performed best with a return exceeding 33%. More tech-focused strategies faced more issues but returned closely below 10% after an extremely successful 2020. Global macro strategies had a tough year and closed only slightly positive for the year. The SMC Global Macro Strategy Index is up almost 37% in 2021, which is largely due to the Discretionary Global Macro Strategy achieving a return of almost 70%. To nobody’s surprise, cryptocurrency strategies performed best in 2021. The SMC Cryptocurrency Strategy Index gained more than 212% in 2021. In the space, it was most important to hold a diversified account of cryptocurrencies to achieve such a great return, as Bitcoin (BTC) gained only 60%. The most successful strategies in the space focused on riskier tokens. The Token and Token Liquid strategies gained 295% and 385% respectively. Despite the great results of 2021, the gains are still inferior to the 342% in 2020. The developments in the crypto space will be discussed in a further paragraph. Lastly, another indicator that the industry is in a healthy state is the fact that the number of launches substantially exceed the liquidations and the number of active funds has reached an all-time high of 22,081.

The most noteworthy event in September 2021 was probably the apparent collapse of Evergrande, one of the largest real estate companies in China, whose status is currently unknown. On Thursday, 16th September 2021, Evergrande issued a statement that it will not be able to repay the outstanding interest payments that day. Following this announcement, the financial market was in substantial stress. Equity markets all around the world lost a few percentage points and volatility spiked. Bond trading was under pressure as well, as Evergrande’s bonds were downgraded and frozen from trading. It sometimes was already referred to the next “Lehman Brothers” case. The volatility the stock has seen since is tremendous, as it lost nearly 80% in the first few days after the announcement. It seemed as though the situation had stabilized, but since not all due payments were paid on Friday, 24th September 2021, the status is unknown. If nothing else happens, which is highly unlikely, the company would enter a grace period following bankruptcy. There are three critical features involved in Evergrande. Firstly, China and Chinese people are heavily engaged with the company, as the company has sold many buildings already without having built them yet. A default would cause huge issues for the affected people. Secondly, many companies are frequently doing business with Evergrande, in particular construction, design and other suppliers, could also face bankruptcy alongside Evergrande. Lastly, the collapse of Evergrande would pose a substantial risk to the financial system of China. The latter one is in particular difficult, as the company has outstanding debt at more than 250 banks, which could put additional pressure on China’s ability to offer cheap debt, which is necessary to maintain growth level. Moreover, it does not make a China a more appealing place to invest for foreign investors, which were already on the decline since the recent developments

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |