|

In this challenging ecosystem, alternative assets showed resilience to the drawdowns in public markets. While some hedge funds have struggled in recent times, the industry is managing the current situation well. For the first time since the pandemic, hedge fund launches have reached pre-pandemic levels again. Regarding performance, in particular large hedge funds have managed the drawdowns well. Figure 2 shows a comparison of public equities and bond indices relative to equity and fixed income hedge funds. For equity strategies, hedge funds were able to mitigate the largest drawdowns of public equities, while also benefitting from the recovery periods (although not to the degree as public equities have). For fixed income strategies, the results are even better. Not only were the funds able to mitigate the drawdowns in fixed income significantly, but they also posted stronger gains in the recovery periods, at least in most instances. Private debt and private equity funds achieved similar results, although it is unknown as of yet how they did in the very short-term. Throughout 2022, private debt funds managed to return a positive performance in each quarter and enhance the stability of a portfolio substantially. Private equity strategies functioned similarly to equity hedge funds, as they mitigated most of the drawdowns of public equity, even for the riskiest sub-strategy in venture capital. Figure 3 shows a comparison of direct lending, private equity, and venture capital benchmark indices versus public equities. While these results are promising, the private equity industry has not been unfazed by the recent crisis. Fundraising became a substantial issue in Q1 2023 as well as more and more downrounds. This leads private equity funds to search for alternatives. One of which seems to be buying back its own debt, which has been more prominent in recent months. Especially in the fundraising department, private debt also saw a substantial shortage, such that pension funds and endowments make up almost 50% of the capital raised. While higher interest rates also lead to higher yields in the private debt markets, it comes at an increased risk with rising loan default rates.

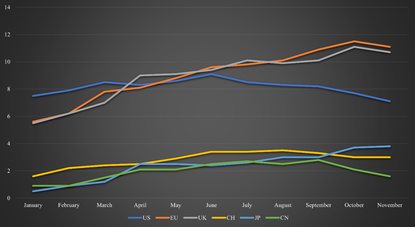

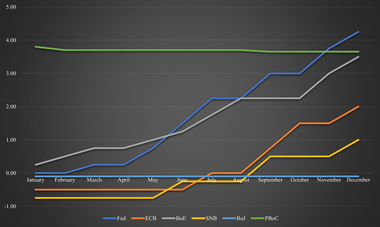

Inflation was a core issue in 2022 and remains to be one in 2023. In the US, inflation started to decline in the summer of 2022 and remains currently at a level of 7.1%. Contrarily, in Europe and the UK, inflation remains a huge issue and has barely declined from its peak in 2022. It remains at 11.1% for the EU and at 10.7% for the UK. The difference between the inflation can largely be attributed to two factors. Firstly, the Fed hikes interest rates more aggressively than its European counterparts. This led to a quicker response to inflation. Secondly, Europe is more directly affected by the war between Russia and Ukraine and is largely dependent on Russian oil and gas, which soared in price following the war. Contrarily to other European countries, Switzerland managed to keep inflation relatively low with a peak in late summer 2022 at 3.5% and 3% currently. Switzerland managed to avoid high inflation due to its strong currency and relatively low demand for fossil fuels, as most of its electricity stems from hydropower and nuclear power. In Asia, both Japan and China also experience limited inflation issues. Japan achieved this through its central bank which continuously intervenes with large-scale monetary easing. Despite the low inflation, Japan is still suffering, as wages remain stagnant unlike in other major economies where it helps offset the higher inflation to some degree. China does not face an inflation problem, due to their different handling of the Covid crisis. Unlike most economies, they did not provide large stimuli to the economy. Additionally, their zero-Covid policy substantially reduced household demands. Figure 1 shows a summary of the inflation rates across the highlighted economies during 2022. Regarding 2023, it is widely expected that inflation, especially in high-inflation countries, will come down. For instance, in the US, it is expected that inflation will be around 4% on average, and close to the 2% Fed target by the end of the year. Inflation forecasts in the EU and the UK are more difficult to estimate, due to their dependency on the war and its outcome. Additionally, unlike in the US, inflation has not really started to decrease. Assuming further strong interventions by the European central banks, it is expected that inflation will drop substantially. The ECB expects the average inflation to be around 5%-6% during 2023 with inflation slightly below 4% by the end of 2023. In the short term, Europe will be under pressure and the measures take time to become effective, as shown in the example of the US. Despite a similar outlook to the US, albeit with a delay of around half a year, it is less promising. One important wildcard is energy prices, which are strongly linked to the war. While the EU managed to get its oil largely from other sources than Russia, it still needs Russia, and gas is not as easily substitutable. With the prospect of Russia’s supply cut and China reopening, prices of energy sources are likely to increase. Depending on the scale, if it occurs, the anticipated target may not be reached and inflation will remain higher than the target. In Switzerland, inflation is expected to remain around the 3% mark for 2023. Given the strong involvement of the BoJ, Japan’s inflation is expected to end the year 2023 below the 2% inflation mark. It is additionally expected that wages will rise for the first time in three decades. Inflation in China is expected to rise to around 2% in 2023. This is a combination of the reopening of the economy and the end of the zero-Covid policy. This will lead to an increase in economic activity and the necessity for further energy. Additionally, the price pressure across will also be felt in China, once demand picks up again. The interest rate hikes by most countries have been another crucial topic during 2022. So far, the hikes have shown limited effectiveness in dealing with soaring inflation. In high-inflation countries, it was effective for the US and had little impact on the European countries. However, this discrepancy is likely due to the steeper hikes in the US and less dependency on the war by the US. The US employed the strongest measures, as it hiked from 0% at the beginning of 2022 to 4.25% at the end of 2022. In contrast, the ECB just started hiking in June 2022 at -0.5%, which increased to 2% by the end of 2022. The BoE employed a mixture of the two. The UK started hiking at the end of 2021 but hiked in smaller steps than the US. Towards the end of 2022, it increased the step size and is currently at 3.5%. Switzerland started hiking earlier than the ECB, despite substantially lower inflation. Switzerland’s prime rate became positive for the first time in years in September 2022. Currently, the prime rate is sitting at 1%. Japan was one of the exceptions, as the BoJ did not hike at all. Its prime rate remains at -0.1%. However, the central bank still strongly intervened in the market as elaborated previously. The People’s Bank of China even lowered its prime lending rate over 2022, albeit to a minimal degree. Currently, the rate is at 3.65%. There is a strong consensus for the year 2023 in the US and Japanese markets. Most market participants expect the Fed to keep raising interest rates to around 5%-5.25%. The Fed is likely to do this in smaller steps than previously. Nonetheless, this level should be reached by the end of Q1 2023. Afterward, a majority of institutions do not expect further hikes or cuts in 2023. The remainder anticipates potential interest rate cuts in Q4 2023. The exact outcome of potentially further hikes or cuts largely depends on the state of the US economy in the latter part of 2023. While the measures seem to be effective and inflation is going down considerably, the risk of a recession is considerable. This largely stems from substantially higher financing costs for businesses, and lower demand from consumers as Covid reserves are exhausted and households feel the pressure from the inflation over the past year. Given that the BoJ has not intervened by raising interest rates, it is not expected that it will in 2023. It is more likely that it will continue its qualitative and quantitative easing philosophy employed so far. In particular, as Japan does not face an imminent inflation problem. With expected wages adjusted, the pressure of inflation should also be eased without a strong necessity to make policy adjustments. For the EU, it is expected that rates will be hiked further to combat the prevalent inflation. Market participants expect interest rates of around 3%, which should be reached during Q2 2023. For the UK, additional hikes of 1% are expected, resulting in interest rates of around 4.5% for 2023. For both economies, no rate cuts are expected in the latter half of 2023. In Switzerland, the SNB is anticipated to hike another 0.5% in 2023 with no rate cuts as well.

Central banks continue to be in the spotlight. Over the past months, it is hard to find a central bank that has not raised interest rates at least once. Inflation remains at four-decade highs in most countries, despite the measures taken by central banks so far. The Fed raised interest rates by another 75bps this month and maintains its stance to aggressively combat inflation. This led the 2-year Treasuries to surge above 4%, for the first time since before the global financial crisis, and increases the likelihood of a recession as well as potentially sharply declining equities. The latest hike increased the federal fund rate to 3% - 3.25%. The ECB also raised its interest rate by 75bps in September, while the Bank of England increased its rate by 50bps. The ECB’s rate is now at 1.25% and the UK’s is at 2.25%. Switzerland also raised its rate by 75bps which brings it into positive territory as the last country in Europe. In the middle East, Saudi Arabia, the UAE, and Qatar follow the Fed with their 75bps hikes as well. Across the developed countries, Japan remains the last country with currently negative rates at -0.10%. September 2022 has also been highly relevant for the currency market. The dollar has strengthened substantially over the year. Compared to the Euro, it appreciated from around 0.9$/€ in 2020 to 1.03$/€. The British Pound declined strongly. The latest tax cut in the UK is threatening even higher inflation and will force the BoE to act more aggressively in tightening. After the announcement, the Pound dropped below 1.1$/£, and some speculate that the Pound could fall below parity to the USD. The Japanese Yen also experienced substantial movements, as the country is buying Yen again for the first time in nearly a quarter century. In spite of the negative developments of equities in 2022 and their even more grim prospect, equities are doing great on a historical scale. Figure 1 shows the growth of global equities with the impact of several crises

Inflation remains a major concern in 2022. It is also crucial to watch the central banks’ responses to deal with it. In particular, the inflation numbers in the coming months should be watched closely, as they likely determine the extent to which central banks intervene. As seen in May 2022, when the CPI was higher than expected, markets lost substantially. With current market expectation of US interest rates being close to 2% later this year, it is vital that the 50bps hike last month, as well as the upcoming hike (likely another 50bps) show effectiveness. If that should not hold, there will be a bumpy road ahead. Especially, as the Fed is starting to reduce its balance sheet, which puts further pressure on markets. A similar observation can be made for the UK. For the EU, this is likely occur a couple of months later, as they have not raised interest rates yet, but are expected to do very soon. This development, alongside the war and supply chain issues, has led to a more and more pessimistic view of GDP growth in most countries. The World Bank expects that most countries will in fact experience a recession. They further emphasize that stagflation is looming. The possibility of a stagflation environment is certainly not unlikely and many factors speak for it. For example, the very high inflation, frequently downward-adjusted GDP projections, and the pressure put on companies with significant supply chain problems among others. Although employment looks healthy in most countries, if this should worsen, the treat of stagflation becomes very urgent. A more detailed view on the macroeconomic situation is provided by Macro Eagle further below. Hedge funds are in a good position to mitigate much of this market volatility. Many hedge funds pursuing equity and fixed income strategies have experienced rough times but they have the capabilities to reduce risk in such a market environment, despite a rather unimpressive performance. Hedge funds that use different strategies than the previously mentioned ones, mostly had a great year. This is in particular true for global macro funds. A substantial number of funds managed to deliver a YTD in 2022 in excess of 100% already. Another strategy that stands out are funds of hedge funds that could truly show their risk mitigation potential. Although private equity and venture capital could not maintain their trend from 2021, the asset class still remains an attractive opportunity. Valuations are down since early 2022. However, the industry is still in a healthy state, despite the slump of public equities. Inflows in the industry are likely to be smaller than in 2021, but there is still significant investor interest as most investors report that their private equity investment substantially outperformed their public equity investments over the long-term. The industry also still sits on a large cash pile amassed over the past year that needs to be deployed. This pressure further mitigates the decline in valuations resulting from the bear market.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |