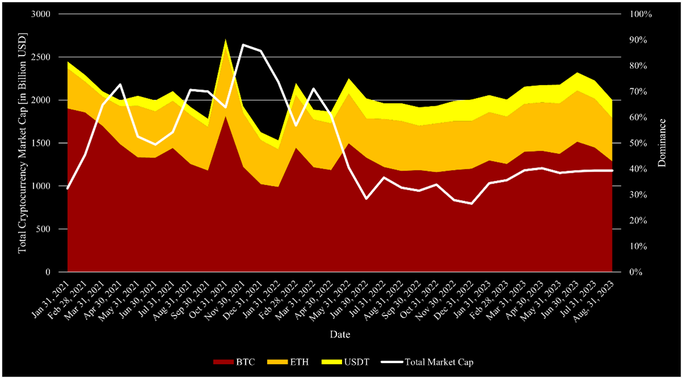

The cryptocurrency markets have been relatively quiet this year. Aside from the surge at the beginning of the year, cryptocurrencies have remained relatively flat since then. The total market capitalization of the industry started slightly below $1tn at the beginning of 2023 and has remained at around $1.2tn since March 2023. The relatively low volatility of the industry also signals a certain level of cautiousness of investors, as the market environment is not great for the industry. In particular recession concerns are holding the industry back, as cryptocurrencies are notorious for sharp declines. Options data on cryptocurrencies also supports a more defensive notion of investors, as implied volatility is close to a record low. The lower degree of risk appetite is also visible in the Bitcoin (BTC) and Ethereum (ETH) dominance. This measure quantifies the total market capital of BTC and ETH respective to the total cryptocurrency market capitalization. Their dominance has been on the rise since Q3 2022 and shows fewer investments in riskier and emerging projects. Similarly, during these times stablecoin gained more importance in the space due to their stability compared to other coins. Figure 1 shows the total market capitalization of cryptocurrencies and the dominance of BTC, ETH, and USDT. Historically, these times are the most important ones for the space, as it drives innovation. With no frenzy, emerging companies are not in a rush to cash out which allows them more time to develop their projects.

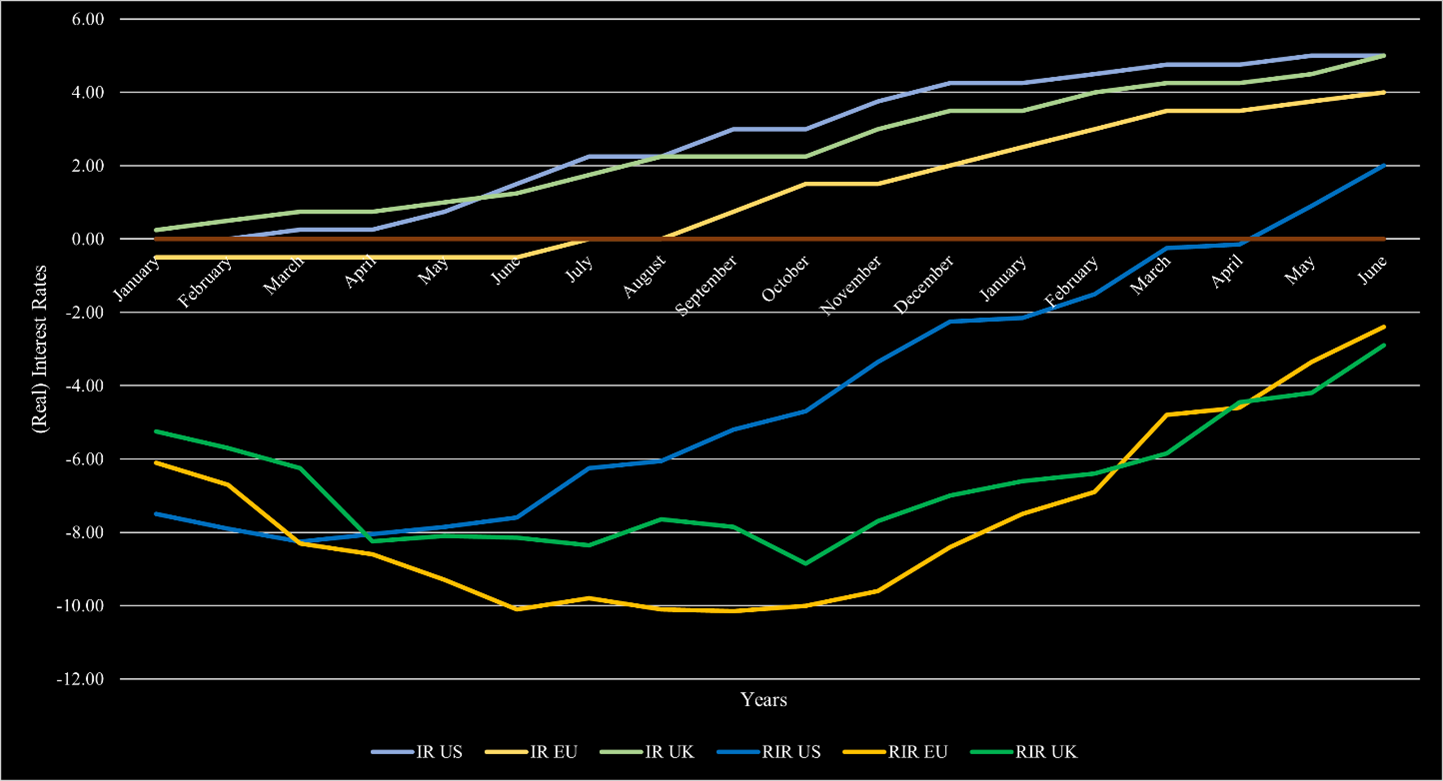

The current economy remains under pressure and recession talks mostly vary based on their expected impact and when they occur. In the US, interest rates remain high at 5.25% with moderate inflation at 3.2%. While inflation seems to normalize, it rose compared to June 2023, which led to another hawkish view of the Fed and further rate hikes are not unlikely. The yield curve inversion of 2Y-10Y yields is especially worrying, as the inversion has persisted for about a year now and economists expected an elevated likelihood of a small to medium recession. In Europe, the situation is more tense, as present headwinds, such as energy and the war in Ukraine, do not seem to evaporate quickly. As a consequence, inflation is coming down more slowly than in the US. In the EU, inflation remains at 6.1% and 6.8% in the UK with interest rates at 4.25% for the EU and 5.25% in the UK. Figure 1 summarizes the development of interest rates and inflation in the US, the EU, and the UK. In Europe, the economic growth is concerning, as the estimated GDP growth in the EU is only 0.6% in Q2 2023. In the UK, the situation is more dire, as the economy has remained close to flat since Q2 2022.

The macroeconomic environment remains challenging for all market participants. Aside from the high volatility in the market, the uncertainty about future interest and inflation rates makes the investment processes much more difficult. In the US, the situation is decent compared to most other countries. Inflation is back at a moderate level of 3.2%, despite the recent increase from 3% in June. However, the interest rate is still very high at 5.25%-5.5%, which adds significant pressure to companies, especially if there is a recession. In the EU, the situation is less promising, as inflation remains above 6% with only slightly lower interest rates at 4.25%-4.5%. Despite this, the EU area is recovering following the development of the US with a delay of a couple of months. It is likely that inflation will be down to manageable levels by the end of 2023, assuming there is no further escalation in the war between Russia and Ukraine. In the UK, the situation is more precarious. Inflation is still close to 8% and has remained above 10% for almost a year. In addition, the BoE’s interest rates are at equal levels as the Fed’s. With an already struggling economy, this only increases the issues. However, the development in the last few months has been positive with inflation coming down. This might ease the immediate pressure, but the economy is still under a lot of pressure. Figure 1 summarizes the development of inflation and interest rates in the US, the EU, and the UK.

The current macroeconomic volatility has not changed. Interest rates and inflation remain elevated. At least in most markets, the inflation rate is continuously declining. In the US, inflation reached 3% and is on its way to the upper target of 2% in the short-term. Europe is following this development but still has a substantial way ahead before inflation will eventually reach those levels, as inflation remains at 6.4%. In the UK, the situation is more dire and inflation declined to 7.9% after being above 10% since August 2022. In order to bring inflation levels down, central banks have hiked substantially over the past 1.5 years. In the US, the federal fund rate is now above 5.25% with the most recent hike, which has largely been deemed unnecessary by market participants. The ECB also increased its interest rate by 25bps and is now at 4.25%. The BoE also raised its core interest rate by 25bps in their latest meeting and is now equivalent to the US’s 5.25%. The US also reached the status of positive real interest rates since the hikes started. Europe and the UK are following this trend but have not reached this territory yet. Figure 1 also shows how Europe and the UK are lacking behind the US. In the current environment, a recession is still likely. While projections have changed throughout the year, the consensus opinion remains that there will likely be a short and with a shallow to medium impact on the economy. The most notable change is that the recession expectation has pushed further and further into the future. It started with estimations that it will happen by mid-2023, then towards the end of 2023. Now, most estimates place the recession somewhen in 2024.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |