Central banks continue to be in the spotlight. Over the past months, it is hard to find a central bank that has not raised interest rates at least once. Inflation remains at four-decade highs in most countries, despite the measures taken by central banks so far. The Fed raised interest rates by another 75bps this month and maintains its stance to aggressively combat inflation. This led the 2-year Treasuries to surge above 4%, for the first time since before the global financial crisis, and increases the likelihood of a recession as well as potentially sharply declining equities. The latest hike increased the federal fund rate to 3% - 3.25%. The ECB also raised its interest rate by 75bps in September, while the Bank of England increased its rate by 50bps. The ECB’s rate is now at 1.25% and the UK’s is at 2.25%. Switzerland also raised its rate by 75bps which brings it into positive territory as the last country in Europe. In the middle East, Saudi Arabia, the UAE, and Qatar follow the Fed with their 75bps hikes as well. Across the developed countries, Japan remains the last country with currently negative rates at -0.10%. September 2022 has also been highly relevant for the currency market. The dollar has strengthened substantially over the year. Compared to the Euro, it appreciated from around 0.9$/€ in 2020 to 1.03$/€. The British Pound declined strongly. The latest tax cut in the UK is threatening even higher inflation and will force the BoE to act more aggressively in tightening. After the announcement, the Pound dropped below 1.1$/£, and some speculate that the Pound could fall below parity to the USD. The Japanese Yen also experienced substantial movements, as the country is buying Yen again for the first time in nearly a quarter century. In spite of the negative developments of equities in 2022 and their even more grim prospect, equities are doing great on a historical scale. Figure 1 shows the growth of global equities with the impact of several crises

Alternative Markets Outlook H2 2022

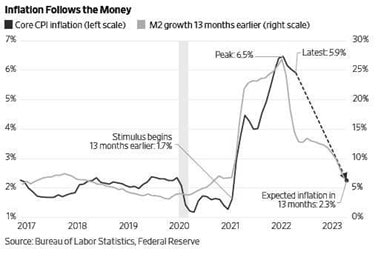

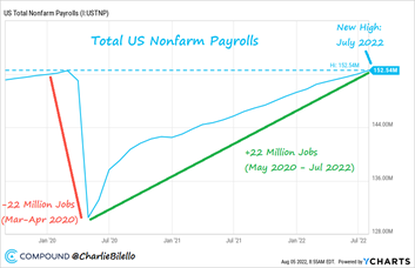

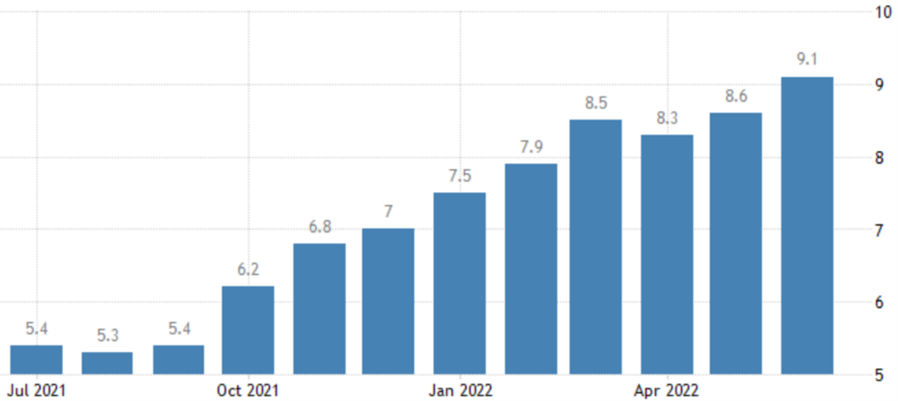

Inflation will likely dominate the news in the latter half of 2022. It is likely to stay high although decreasing. Exact predictions are always difficult, especially in such a market environment. This is also observable in the research from economists who struggle to predict accurately, as employment is high, GDP is shrinking, and the current inflation issues. Whether inflation will in fact slow down is largely dependent on the ongoing war between Russia and the Ukraine, as energy and food are the main drivers behind the current inflation levels. Regardless of how the war ends, even if soon, there is a low chance that the energy supply of Russia to Europe will ramp up significantly. There may be some help from the OPEC+ countries in alleviating the problem but high energy prices are obviously beneficial for them. Food inflation on the other hand is likely to go down to some degree, as the Ukraine is a key supplier assuming that it remains independent. The energy situation will get very tense during the winter, as Europe is expecting energy shortages. It is likely that energy inflation will spike there. Afterward, in early and mid-2023, the situation likely will improve. At that point, energy prices have a chance to enter a deflationary state, as inflation is measured on a year-on-year basis, in particular when considering that energy inflation is higher than 40% in the US for example. The remaining subcategories in inflation measures are more affected by actual central bank measures. In particular, the US and the UK have taken substantial measures to combat current inflation. At least in the US, the measures have relieved some of the pressure as the monthly inflation fell for the time in a couple of months. However, this does not ease the pressure, as such events must be persistent. It is likely that this will continue, especially if the Fed keeps rising its interest rates, which some of the board members intend to do. It is expected that inflation will keep going down during 2022 and 2023. Frequently expected intervals estimate inflation to be between 2% and 4% towards the end of this period. Figure 1 shows expectations for the core CPI in the year 2023 alongside a lagged M2 growth measure. In Europe, the situation in terms of food and energy is more dire, due to its direct reliance on Russia. However, energy inflation surprisingly is lower than in the US but is rapidly growing, especially with the current concerns about the winter ahead. In terms of central bank measures, it becomes a bit more tricky, as the ECB has to manage many countries and consider their economic situation. This is where its major problem occurs, as large countries, such as Italy, are in a dangerous position. Its debt level is extremely high and it is potentially at risk of defaulting if interest rates should rise. On the other hand, the ECB has to combat the ever-soaring inflation by rising the interest rates. This dilemma will likely reduce the ECB's capabilities to combat inflation by rising interest rates as the UK or the US did. Most likely, this will cause inflation to be mitigated slower and to a lower degree. It is therefore expected that inflation in Europe will still rise in the latter half of 2022 and decline slower than in the US or the UK. This assumption is based on a status quo-like ongoing war. Nonetheless, sudden events can massively alter this outcome. Contrary to the outlook of Europe, the US’s development in July 2022 is largely positive. Firstly, it managed to reduce inflation slightly for the first time in multiple months. Secondly, US employment is back at pre-Covid levels and at the highest since 1969. While the economy lost 22 million jobs in the first two months of the Covid outbreak, in July 2022, it regained all of them. The impressive recovery is shown in Figure 2.

Alternative Markets Summary H1 2022

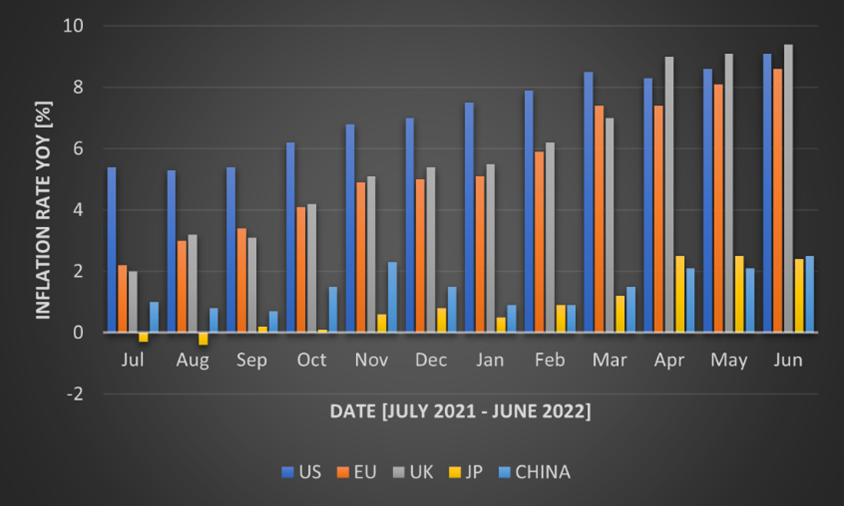

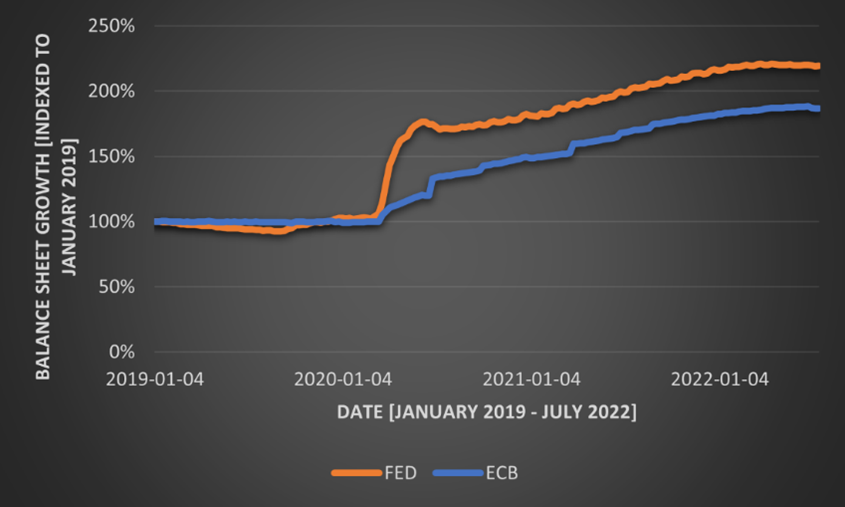

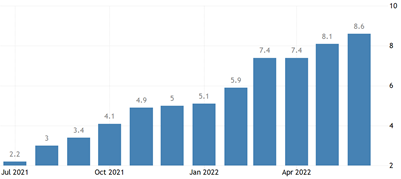

Ever since Covid-19 has subsided from the daily news, inflation has taken over. Inflation is still a major concern in the current economy. This is further exacerbated by central bank interventions that have not been fruitful yet. An additional major contributor is the ongoing war between Russia and Ukraine. As of June 2022, inflation in the US is at 9.1%, the highest it has been in the past 40 years. In the Eurozone, inflation is slightly lower at 8.6%. The UK’s inflation is even higher at 9.4%. Asian countries, such as Japan and China, managed to keep their inflation relatively low at 2.4% and 2.5%. The development of inflation over the past year is summarized in Figure 1. For Western countries, inflation has more or less continuously risen. The US started the year with inflation close to over 5%, while European countries were close to 2%. Nonetheless, Europe has caught up to the US since April, when the UK’s inflation even got higher than the US’s. A potential reason for the higher inflation in the US at the beginning of the year and back until the latter half of 2021 is the rapid and steep unconventional measures taken by the Fed. This faster intervention led to more money being in the economy earlier, which theoretically should lead to higher inflation earlier. Figure 2 shows the growth in the balance sheet indexed to January 2019. Once Covid-19 hit the economy, the US reacted a lot faster and in higher magnitudes than Europe did. Within the first months, the Fed’s balance sheet grew by almost 70%, while the ECB’s only grew by 25% in the same time frame. Since then, the two central banks acted equivalently in terms of balance sheet growth. Very recently, the central banks started to shrink their balance sheets. These measures were announced during Q2 2022 and are slowly implemented. Going forward, this balance sheet shrinking will be strengthened, which is confirmed by an announcement from the ECB recently. Nonetheless, as the graph shows, these measures barely affect the original measures taken to combat the economic consequences of Covid-19. The low inflation in China largely stems from the consequences of their zero-Covid policy. In recent months, many places have been shut down to control the spread of Covid. This led to low production levels and low demand which is reflected in the low inflation levels of the country. In the case of Japan, inflation of above 2% is significant, as the average inflation during the past three decades was only 0.3%. Its inflation largely stems from the consequences of the war and the impact it has on food and energy.

Macroeconomic factors continue to dominate financial markets. Inflation in the US keeps rising, despite attempts of the Fed to slow it down. In June, inflation rose to 9.1%, higher than the anticipated 8.8%. Figure 1 summarizes the development of inflation over the past year in the US. The major drivers remain food and energy, but these are not the only issues. As the prior two are global issues, it is unlikely that those factors will slow down quickly. The Russia-Ukraine war has a substantial impact on those factors. Russia, a key supplier of energy, has led to the possibility of Europe not being able to use as much energy for heating in the winter as usual. Ukraine, which is a key supplier of food, e.g., wheat, puts further pressure on food prices. That Russia started burning down acres does not help the matter either. Although this has no direct impact on the US, the impact on the price of those goods is a significant contributor to the increased prices of those goods. This development has caused markets to anticipate an even larger hike in the upcoming July meeting. Markets analysts now see a hike of an entire percentage point as possible. This further emphasizes how dire the situation looks, as a few months ago, the discussions were between no hikes, a 25 bp, or at worst a 50bp hike. The US federal fund rate is now at 1.75% and likely to rise substantially. Despite these increases, inflation hit a record high (within the past four decades) in June 2022. With this in mind, voices of a looming recession are increasing. The fact that the yield curve inversion between 2y and 10y-Treasuries is at its highest since 2000, does not help mitigate this threat. Figure 2 shows the recent inversion of the two Treasury yields. This recession indicator should not be considered too much, as depending on which maturities are compared, the implications look very different. In Europe, the situation is even more serious. Not only is the continent directly affected by the war and its possibly horrendous outcomes, but it is also susceptible to possible bottlenecks for both energy (in particular gas) and food. Additionally, EU inflation hit a new record of 8.6% in June 2022 without any central bank interventions yet. The development of inflation in the EU is shown in Figure 3.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |