Inflation remains a major concern in 2022. It is also crucial to watch the central banks’ responses to deal with it. In particular, the inflation numbers in the coming months should be watched closely, as they likely determine the extent to which central banks intervene. As seen in May 2022, when the CPI was higher than expected, markets lost substantially. With current market expectation of US interest rates being close to 2% later this year, it is vital that the 50bps hike last month, as well as the upcoming hike (likely another 50bps) show effectiveness. If that should not hold, there will be a bumpy road ahead. Especially, as the Fed is starting to reduce its balance sheet, which puts further pressure on markets. A similar observation can be made for the UK. For the EU, this is likely occur a couple of months later, as they have not raised interest rates yet, but are expected to do very soon. This development, alongside the war and supply chain issues, has led to a more and more pessimistic view of GDP growth in most countries. The World Bank expects that most countries will in fact experience a recession. They further emphasize that stagflation is looming. The possibility of a stagflation environment is certainly not unlikely and many factors speak for it. For example, the very high inflation, frequently downward-adjusted GDP projections, and the pressure put on companies with significant supply chain problems among others. Although employment looks healthy in most countries, if this should worsen, the treat of stagflation becomes very urgent. A more detailed view on the macroeconomic situation is provided by Macro Eagle further below. Hedge funds are in a good position to mitigate much of this market volatility. Many hedge funds pursuing equity and fixed income strategies have experienced rough times but they have the capabilities to reduce risk in such a market environment, despite a rather unimpressive performance. Hedge funds that use different strategies than the previously mentioned ones, mostly had a great year. This is in particular true for global macro funds. A substantial number of funds managed to deliver a YTD in 2022 in excess of 100% already. Another strategy that stands out are funds of hedge funds that could truly show their risk mitigation potential. Although private equity and venture capital could not maintain their trend from 2021, the asset class still remains an attractive opportunity. Valuations are down since early 2022. However, the industry is still in a healthy state, despite the slump of public equities. Inflows in the industry are likely to be smaller than in 2021, but there is still significant investor interest as most investors report that their private equity investment substantially outperformed their public equity investments over the long-term. The industry also still sits on a large cash pile amassed over the past year that needs to be deployed. This pressure further mitigates the decline in valuations resulting from the bear market.

Hedge Funds

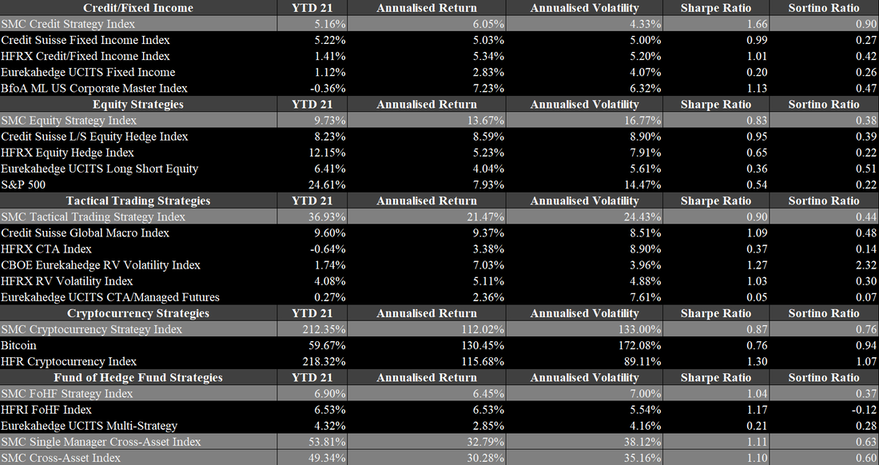

Hedge funds had a great 2021 and managed to set a record high in its AuM. As of the third quarter in 2021, the AuM of the industry is expected to be between $4.3tn and $4.6tn depending on the sources. According to BarclayHedge, the industry’s AuM just surpassed the $4.5tn mark at the end of the third quarter. This is a steep increase from just $3.8tn in 2020, as shown in Figure 6. This is a gain of more than 18% in less than a year. It is expected that the number will rise slightly, once the Q4 2021 numbers are out, as October and November 2021 were rather positive. Nonetheless, December 2021 will have dampened the results of Q4 2021. Generally, the industry has gained substantially over the past ten years, despite a rather inferior view from market participants during most of that period. The AuM soared thanks to two reasons. Firstly, the industry saw substantial capital net inflows. During the first three quarters, the industry received $41bn in fresh capital after having received another $19bn in the second half of 2020. Since then, the industry saw net inflows in every quarter, which is stark break from previous years when the industry experienced net outflows in most quarters. In Q4 2021, net inflows rose to $81bn in 2021, according to Eurekahedge. Figure 7 also shows the severe initial impact of Covid-19 in 2020, when accounting for the significantly positive inflows in the latter half of the year. The second reason for the steep increase in AuM is due to the performance of the hedge fund industry in 2021. Hedge funds in 2021 returned slightly more than 10%, making it the third best year in history after 2020 and 2009 according to HFR. This is remarkable, as the year has not been easy with the constant uncertainty and high volatility in the market. In particular event-driven, equity and commodity strategies have performed very well and the high beta strategies within their respective sector. Figure 8 summarizes the performances of several strategies during 2021 by Eurekahedge. Distressed debt and event-driven strategies performed best with barely any negative performances during the year. Macro and fixed income strategies struggled the most throughout the year, due to the harsh economic conditions. When looking at the highlighted percentiles, it is evident that the high volatility in the market also caused high volatility in hedge fund returns, independent of the strategy. This is most relevant for long short equity strategies whose returns vary between +30% (upper percentile) and -10% (lower percentile) in 2021. Figures 9 to 13 highlight the SMC Strategy Indices in 2021 compared to their benchmarks. The SMC Credit Strategy Index gained slightly more than 5% in 2021, although the variation across strategies is substantial. Two strategies, Trade Finance Crypto and European High Yield L/S Credit did very well in the economic environment, as they reached returns above 12% and 19% in 2021. The Trade Finance Strategy is in particular remarkable, as the strategy has not experienced a negative month since its inception in 2017. The SMC Equity Strategy Index gained closely less than 10%, which is around as much as the average equity strategy in 2021. Within the sector, there was also considerable volatility, due to the sub-strategies. Unsurprisingly, the Equities US Activist Event-Driven performed best with a return exceeding 33%. More tech-focused strategies faced more issues but returned closely below 10% after an extremely successful 2020. Global macro strategies had a tough year and closed only slightly positive for the year. The SMC Global Macro Strategy Index is up almost 37% in 2021, which is largely due to the Discretionary Global Macro Strategy achieving a return of almost 70%. To nobody’s surprise, cryptocurrency strategies performed best in 2021. The SMC Cryptocurrency Strategy Index gained more than 212% in 2021. In the space, it was most important to hold a diversified account of cryptocurrencies to achieve such a great return, as Bitcoin (BTC) gained only 60%. The most successful strategies in the space focused on riskier tokens. The Token and Token Liquid strategies gained 295% and 385% respectively. Despite the great results of 2021, the gains are still inferior to the 342% in 2020. The developments in the crypto space will be discussed in a further paragraph. Lastly, another indicator that the industry is in a healthy state is the fact that the number of launches substantially exceed the liquidations and the number of active funds has reached an all-time high of 22,081.

Just before the holiday season, Omicron is spreading rapidly around the world and causes most countries to impose further restrictions. The Netherlands went furthest with a new lockdown over the Christmas holidays. Due to the high infection rate of Omicron, many countries are recommending booster vaccinations for their citizens and introducing requirements of being vaccinated and negatively tested in an attempt to slow down the spread of the virus. This is not the only issue at the moment, as inflation rates are surging around the world. It is also estimated that inflation will remain high for longer than just a few months. In the US, the CPI has reached 6.8% in November 2021, up from 5.3% in August 2021. In Europe, the CPI is 4.9% in November, up from only 3% in August 2021. The situation is similar in the UK with 4.6% in November 2021. Equity markets have strongly profited from the strong interventions of central banks, as shown in Figure 1. After October 2021, equity markets did not maintain their strong upward trend. When Omicron emerged, equity markets dipped. Nonetheless, after it was thought initially that Omicron can be handled to some degree, markets recovered. This recovery only persisted for a short time, as the further restrictions around the world quickly made the illusion of Omicron being handled perish quickly. This strong performance of the public equity market has fuelled the private market. In particular, technology, healthcare and fintech were of tremendous interest. Figure 2 shows a summary of the growth of fintech in 2021. M&A and SPACs achieved a transaction volume of $337bn and several notable IPOs or direct listings have taken place. This includes Coinbase, Robinhood and Nubank among others. Figure 3 shows the development of fundraising in private markets since 2008. In 2021, almost $1tn in capital was raised by private equity, private debt, real estate and infrastructure. This year’s fundraising is the second largest only after 2019. By far the largest contributor is private equity with more than $600bn raised in 2021. Figure 4 shows the increase in AuM of private markets. In 2021, private markets have surpassed the $10tn threshold. In 2021, a substantial increase in allocated capital took place, as dealmaking was difficult in 2020. The fundraising in 2021 also caused the dry powder to remain high despite large commitments. Most of the assets are managed by the private equity industry and other types of assets.

The most noteworthy event in September 2021 was probably the apparent collapse of Evergrande, one of the largest real estate companies in China, whose status is currently unknown. On Thursday, 16th September 2021, Evergrande issued a statement that it will not be able to repay the outstanding interest payments that day. Following this announcement, the financial market was in substantial stress. Equity markets all around the world lost a few percentage points and volatility spiked. Bond trading was under pressure as well, as Evergrande’s bonds were downgraded and frozen from trading. It sometimes was already referred to the next “Lehman Brothers” case. The volatility the stock has seen since is tremendous, as it lost nearly 80% in the first few days after the announcement. It seemed as though the situation had stabilized, but since not all due payments were paid on Friday, 24th September 2021, the status is unknown. If nothing else happens, which is highly unlikely, the company would enter a grace period following bankruptcy. There are three critical features involved in Evergrande. Firstly, China and Chinese people are heavily engaged with the company, as the company has sold many buildings already without having built them yet. A default would cause huge issues for the affected people. Secondly, many companies are frequently doing business with Evergrande, in particular construction, design and other suppliers, could also face bankruptcy alongside Evergrande. Lastly, the collapse of Evergrande would pose a substantial risk to the financial system of China. The latter one is in particular difficult, as the company has outstanding debt at more than 250 banks, which could put additional pressure on China’s ability to offer cheap debt, which is necessary to maintain growth level. Moreover, it does not make a China a more appealing place to invest for foreign investors, which were already on the decline since the recent developments

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |