Alternative Markets Summary H1 2022

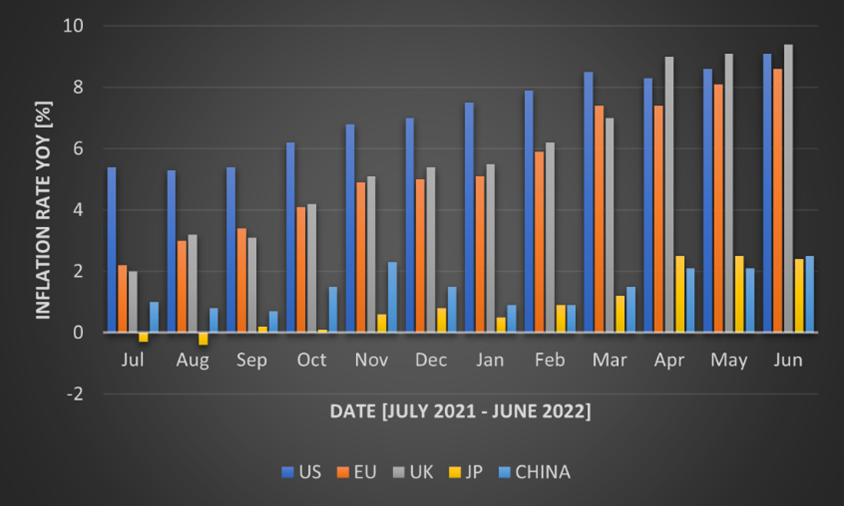

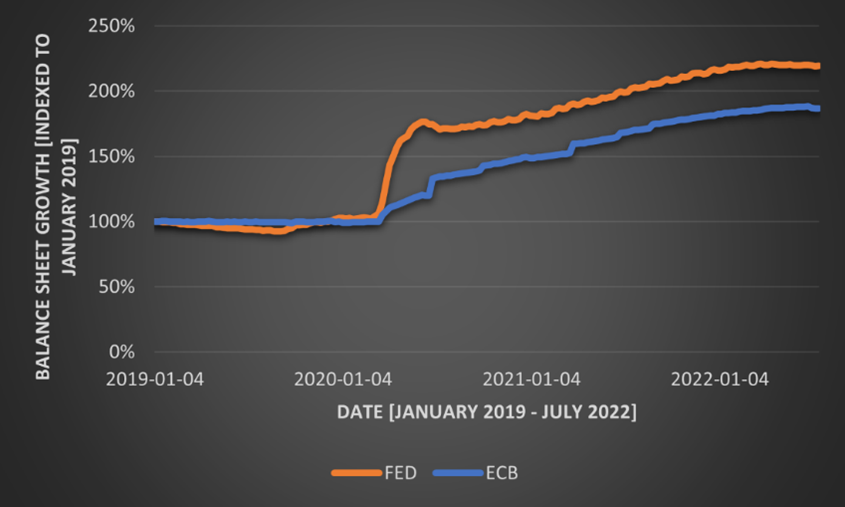

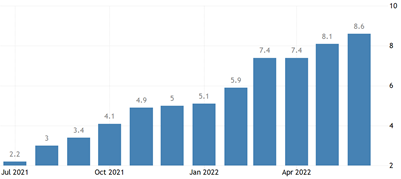

Ever since Covid-19 has subsided from the daily news, inflation has taken over. Inflation is still a major concern in the current economy. This is further exacerbated by central bank interventions that have not been fruitful yet. An additional major contributor is the ongoing war between Russia and Ukraine. As of June 2022, inflation in the US is at 9.1%, the highest it has been in the past 40 years. In the Eurozone, inflation is slightly lower at 8.6%. The UK’s inflation is even higher at 9.4%. Asian countries, such as Japan and China, managed to keep their inflation relatively low at 2.4% and 2.5%. The development of inflation over the past year is summarized in Figure 1. For Western countries, inflation has more or less continuously risen. The US started the year with inflation close to over 5%, while European countries were close to 2%. Nonetheless, Europe has caught up to the US since April, when the UK’s inflation even got higher than the US’s. A potential reason for the higher inflation in the US at the beginning of the year and back until the latter half of 2021 is the rapid and steep unconventional measures taken by the Fed. This faster intervention led to more money being in the economy earlier, which theoretically should lead to higher inflation earlier. Figure 2 shows the growth in the balance sheet indexed to January 2019. Once Covid-19 hit the economy, the US reacted a lot faster and in higher magnitudes than Europe did. Within the first months, the Fed’s balance sheet grew by almost 70%, while the ECB’s only grew by 25% in the same time frame. Since then, the two central banks acted equivalently in terms of balance sheet growth. Very recently, the central banks started to shrink their balance sheets. These measures were announced during Q2 2022 and are slowly implemented. Going forward, this balance sheet shrinking will be strengthened, which is confirmed by an announcement from the ECB recently. Nonetheless, as the graph shows, these measures barely affect the original measures taken to combat the economic consequences of Covid-19. The low inflation in China largely stems from the consequences of their zero-Covid policy. In recent months, many places have been shut down to control the spread of Covid. This led to low production levels and low demand which is reflected in the low inflation levels of the country. In the case of Japan, inflation of above 2% is significant, as the average inflation during the past three decades was only 0.3%. Its inflation largely stems from the consequences of the war and the impact it has on food and energy.

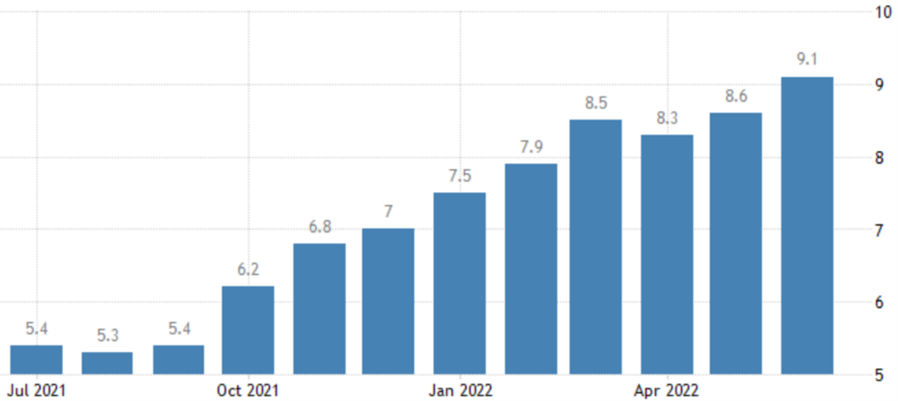

Macroeconomic factors continue to dominate financial markets. Inflation in the US keeps rising, despite attempts of the Fed to slow it down. In June, inflation rose to 9.1%, higher than the anticipated 8.8%. Figure 1 summarizes the development of inflation over the past year in the US. The major drivers remain food and energy, but these are not the only issues. As the prior two are global issues, it is unlikely that those factors will slow down quickly. The Russia-Ukraine war has a substantial impact on those factors. Russia, a key supplier of energy, has led to the possibility of Europe not being able to use as much energy for heating in the winter as usual. Ukraine, which is a key supplier of food, e.g., wheat, puts further pressure on food prices. That Russia started burning down acres does not help the matter either. Although this has no direct impact on the US, the impact on the price of those goods is a significant contributor to the increased prices of those goods. This development has caused markets to anticipate an even larger hike in the upcoming July meeting. Markets analysts now see a hike of an entire percentage point as possible. This further emphasizes how dire the situation looks, as a few months ago, the discussions were between no hikes, a 25 bp, or at worst a 50bp hike. The US federal fund rate is now at 1.75% and likely to rise substantially. Despite these increases, inflation hit a record high (within the past four decades) in June 2022. With this in mind, voices of a looming recession are increasing. The fact that the yield curve inversion between 2y and 10y-Treasuries is at its highest since 2000, does not help mitigate this threat. Figure 2 shows the recent inversion of the two Treasury yields. This recession indicator should not be considered too much, as depending on which maturities are compared, the implications look very different. In Europe, the situation is even more serious. Not only is the continent directly affected by the war and its possibly horrendous outcomes, but it is also susceptible to possible bottlenecks for both energy (in particular gas) and food. Additionally, EU inflation hit a new record of 8.6% in June 2022 without any central bank interventions yet. The development of inflation in the EU is shown in Figure 3.

Inflation remains a major concern in 2022. It is also crucial to watch the central banks’ responses to deal with it. In particular, the inflation numbers in the coming months should be watched closely, as they likely determine the extent to which central banks intervene. As seen in May 2022, when the CPI was higher than expected, markets lost substantially. With current market expectation of US interest rates being close to 2% later this year, it is vital that the 50bps hike last month, as well as the upcoming hike (likely another 50bps) show effectiveness. If that should not hold, there will be a bumpy road ahead. Especially, as the Fed is starting to reduce its balance sheet, which puts further pressure on markets. A similar observation can be made for the UK. For the EU, this is likely occur a couple of months later, as they have not raised interest rates yet, but are expected to do very soon. This development, alongside the war and supply chain issues, has led to a more and more pessimistic view of GDP growth in most countries. The World Bank expects that most countries will in fact experience a recession. They further emphasize that stagflation is looming. The possibility of a stagflation environment is certainly not unlikely and many factors speak for it. For example, the very high inflation, frequently downward-adjusted GDP projections, and the pressure put on companies with significant supply chain problems among others. Although employment looks healthy in most countries, if this should worsen, the treat of stagflation becomes very urgent. A more detailed view on the macroeconomic situation is provided by Macro Eagle further below. Hedge funds are in a good position to mitigate much of this market volatility. Many hedge funds pursuing equity and fixed income strategies have experienced rough times but they have the capabilities to reduce risk in such a market environment, despite a rather unimpressive performance. Hedge funds that use different strategies than the previously mentioned ones, mostly had a great year. This is in particular true for global macro funds. A substantial number of funds managed to deliver a YTD in 2022 in excess of 100% already. Another strategy that stands out are funds of hedge funds that could truly show their risk mitigation potential. Although private equity and venture capital could not maintain their trend from 2021, the asset class still remains an attractive opportunity. Valuations are down since early 2022. However, the industry is still in a healthy state, despite the slump of public equities. Inflows in the industry are likely to be smaller than in 2021, but there is still significant investor interest as most investors report that their private equity investment substantially outperformed their public equity investments over the long-term. The industry also still sits on a large cash pile amassed over the past year that needs to be deployed. This pressure further mitigates the decline in valuations resulting from the bear market.

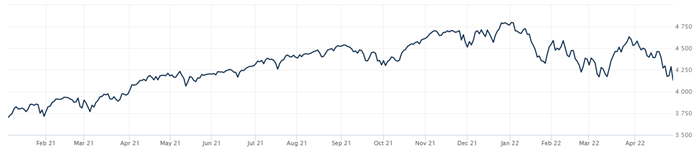

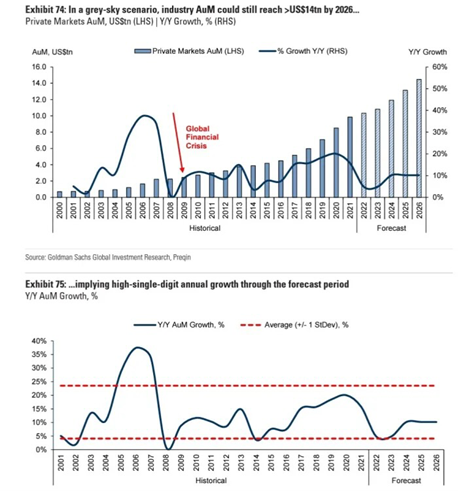

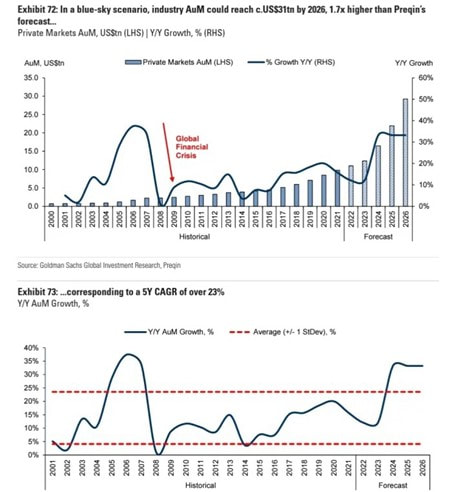

Markets are continuing to struggle in 2022. Equity markets have suffered substantial losses after their stellar 2021 caused by a combination of inflation, (expected) interest rate hikes and the Russia-Ukraine war. After the strong selloff at the end of April 2022 which closed the worst monthly performance since the financial crisis, equity indices are down substantially. The S&P500 is down almost 14% YTD while the tech-driven Nasdaq index is down more than 21%. The development of the S&P500 since January 2021 is shown in Figure 1 below. After its record high from the end of 2021, the index is as low as one year ago. Although equities are still high from a historical perspective, the anticipated, and very likely, interest rate hikes from the Fed are on the horizon. It is anticipated that the Fed will increase rates by 0.5% in May and possibly another 0.5% in June. This has a substantial impact on still highly valued stocks which will put further pressure on equities. Central banks are feeling the consequences of their extensive interventions during Covid-19. It led to record inflation levels (at least of the last 40 years), and the imminent treat of recession if interest rates are increased. Nonetheless, if interest rates are not increased, inflation could spiral out of control, if it has not already. Given that inflation has reached 8.5% in the US and 7.4% in Europe, the necessity to intervene is obvious. These difficult times are another opportunity for hedge funds to prove their worth, as they have since Covid-19. Despite losses of the industry collectively during Q1 2022, the industry still sees continued inflows. The difficulties from the uncertainties at the current moment make hedge fund selection more important, as the gap between good and bad hedge funds widened. Given the current market situation, equity-neutral, global macro and commodity-based strategies achieved great results. In particular our Discretionary Global Macro strategy had a phenomenal month with a gain of more than 50% in March and a gain of almost 150% in Q1 2022. Our crypto- and equity strategies did well in March 2022 and could partially offset their loss from earlier in the year. Nonetheless, this is unlikely to continue in April, due to the selloff in both markets at the end of the month. Another great alternative to be partially shielded to current market volatility is private equity and venture capital. Although both markets benefitted greatly from the overheated public markets in the past two years, valuations have declined slightly. Regardless of the decline in valuations, there is still a huge interest in the space as money keeps flowing in and the deal activity is very high in the space. The large amount of capital in the space alongside the competition are also likely to prevent such large decreases as the public equity markets see currently. Both of these markets, hedge funds and private equity, are large drivers of alternative markets. According to research from Goldman Sachs and Preqin, the AuM will significantly increase, even in a suboptimal ecosystem. In a grey-sky scenario, they expect the industry to grow to $14tn in 2026, up from $10tn in 2021. In a more favourable blue-sky scenario, they expect the AuM to rise to $31tn in the same time frame. Figures 2 and 3 show their findings.

|

|

RSS Feed

RSS Feed

|

|

|

Stone Mountain Capital LTD is authorised and regulated with FRN: 929802 by the Financial Conduct Authority (‘FCA’) in the United Kingdom. The website content is neither an offer to sell nor a solicitation of an offer to buy an interest in any investment or advisory service by Stone Mountain Capital LTD and should be read with the DISCLAIMER. © 2024 Stone Mountain Capital LTD. All rights reserved. |